Page 2 of 4

Re: Selling Unilever?

Posted: September 12th, 2019, 7:36 am

by Darka

monabri wrote:As mentioned by other Lemons above, if one considers the Total Return for Unilever over the last 5 years versus FCIT, HFEL,WTAN, CTY, BA. & HFEL, it has outperformed all of them - the likes of BA., CTY & even HFEL by some margin. Of course, past performance etc.

Hi monabri,

How did you create those graphs by the way?

Re: Selling Unilever?

Posted: September 12th, 2019, 1:29 pm

by monabri

Darka wrote:monabri wrote:As mentioned by other Lemons above, if one considers the Total Return for Unilever over the last 5 years versus FCIT, HFEL,WTAN, CTY, BA. & HFEL, it has outperformed all of them - the likes of BA., CTY & even HFEL by some margin. Of course, past performance etc.

Hi monabri,

How did you create those graphs by the way?

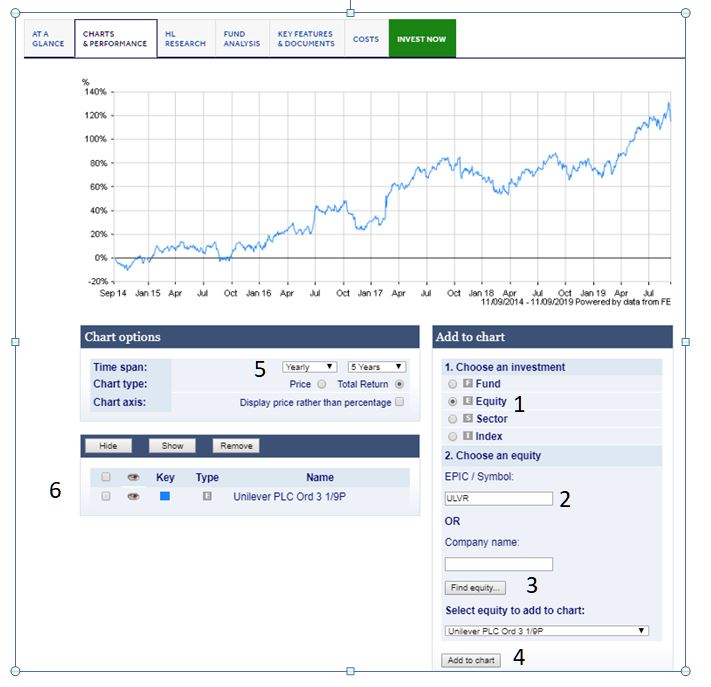

I use the HL tools here:-

https://www.hl.co.uk/funds/fund-discoun ... ion/chartsYou can compare up to 7 shares/funds at a time.

1- Click on "Equity"

2- Type in the ticker ...in this case ULVR for Unilever

3- Find Equity

4 - Add to chart

5- Select the timescale and Total Return

6 - to remove a curve, check the square box and "remove"

Re: Selling Unilever?

Posted: September 12th, 2019, 2:07 pm

by Arborbridge

ULVR, RB and DGE tend to bring up the same questions for me. Each time I go through the various arguments for and against, and each time they survive, partly owing to my own inertia.

I usually question the wisdom of holding them when I book the dividends and realise how piffling they are compared with other companies. Then, if I top slice, naturally the dividends get even smaller.

Still, they are good core businesses, and when I look at the TR, it's not to be sneezed at. And so to sleep until the next time the question comes up.....

Arb.

Re: Selling Unilever?

Posted: September 12th, 2019, 3:01 pm

by Dod101

They are certainly not High Yield shares, any of them, and so inappropriate for discussion here, but then the OP was considering selling. UK high yield shares have been pretty hopeless investments in rebent years unless we are totally focussed on yield and are prepared to ignore the share price, but that is why I hold Unilever and Diageo, ( the latter being a recent addition to my portfolio). In contrast, they have an excellent record of total return.

Dod

Re: Selling Unilever?

Posted: September 12th, 2019, 3:22 pm

by richfool

Arborbridge wrote:ULVR, RB and DGE tend to bring up the same questions for me. Each time I go through the various arguments for and against, and each time they survive, partly owing to my own inertia.

I usually question the wisdom of holding them when I book the dividends and realise how piffling they are compared with other companies. Then, if I top slice, naturally the dividends get even smaller.

Still, they are good core businesses, and when I look at the TR, it's not to be sneezed at. And so to sleep until the next time the question comes up.....

Arb.

Yes, all good points.

I too have recently top-sliced (well sold half my holding) ULVR and the dividend I've just received has thus got even smaller.

I am also conscious of the concept of better performing stocks reverting to the mean.

So I am pondering whether to sell the remainder and chuck the proceeds into one of the UK G&I IT's that I hold, either CTY, FGT, MUT or TIGT., - all hold ULVR anyway, - or even to top up a Global G&I or Multi-Asset trust, all of which provide a higher yield and greater diversification/less risk.

Re: Selling Unilever?

Posted: September 12th, 2019, 6:39 pm

by ADrunkenMarcus

If selling Unilever is the answer, you've asked the wrong question.

Best wishes

Mark.

Re: Selling Unilever?

Posted: September 12th, 2019, 6:47 pm

by TUK020

the problem with super reliable growth shares, that have a lower yield (but which is tolerable due to earnings growth) is when the growth stops, and they fall off their 'quality earnings' pedestal, and then get de-rated by the market.

thinking RR, RB, Tesco, Cobham, etc as some of my own scar tissue.

I like TJH's top slicing method, and have managed to top slice NG at 1100, BA at 650, AZN at 6000, MARS at 125. Sure I could run the whole stack for longer, but take comfort in 'banking some profits' for redeployment.

Having said that, don't have Unilever - wife has a stack from employee sharesave which gives us more than enough exposure

Re: Selling Unilever?

Posted: September 12th, 2019, 7:27 pm

by Dod101

Having held Unilever for more than 20 years without change, it was a bit of a shock to my system to sell some but they had reached a stage where they were overwhelmingly the largest holding I had so sold about 20% at £50. I have no intention of selling any more unless they reach £70 when I might sell a few more.

I just leave them alone, ticking away in the background. We all need this sort of share as a foundation. Others like it are Diageo, Royal Dutch Shell and maybe the two big pharmas. They are not all high yield but so what?

Dod

Re: Selling Unilever?

Posted: September 12th, 2019, 8:04 pm

by Spet0789

Why not just sell 2% every year if you want the income?

Hey presto, a 5% income yield and I suspect the total return would still outperform a few of the usual suspects with ‘natural’ 5% yields.

Re: Selling Unilever?

Posted: September 12th, 2019, 9:43 pm

by Alaric

Spet0789 wrote:Why not just sell 2% every year if you want the income?

That is a straightforward solution provided you don't hold the stock in certificated form. If income from the share is just being reinvested to increase your equity holdings, you may as well leave it in Unilever to grow until you become uncomfortable about having too much of your wealth tied to the fortunes of one company.

Re: Selling Unilever?

Posted: September 13th, 2019, 3:47 pm

by tjh290633

TUK020 wrote:the problem with super reliable growth shares, that have a lower yield (but which is tolerable due to earnings growth) is when the growth stops, and they fall off their 'quality earnings' pedestal, and then get de-rated by the market.

thinking RR, RB, Tesco, Cobham, etc as some of my own scar tissue.

I like TJH's top slicing method, and have managed to top slice NG at 1100, BA at 650, AZN at 6000, MARS at 125. Sure I could run the whole stack for longer, but take comfort in 'banking some profits' for redeployment.

Having said that, don't have Unilever - wife has a stack from employee sharesave which gives us more than enough exposure

This stirred me to have a look at the shares which I have trimmed back over the years. I make it 33 of the shares which I have held have been trimmed at some time or other. 1997 was the first occasion, Lloyds and Zeneca being the shares. Then in 1999 BT, Marconi and Prudential got the treatment. In 2000 Blue Circle (twice) and Marconi again. In 2002 it was the turn of Imperial Tobacco (twice) and Tate. In 2003 Stagecoach, RSA and Mitchells & Butler's turn. In 2005 Whitbread and intl. Hotels. In 2006 Pilkington and Scottish Power, followed by Vodafone in 2007. Then, in 2008-9, all hell was let loose, with 14 trimmed in 2008 and 10 in 2009. I will refrain from listing more, but I think IMT holds the record with 7 interventions, including selling rights to avoid the need for trimming.

Unilever has never been trimmed, but Reckitt Benckiser was in 2016. Diageo has been close to it, but fell back. A lot of the trimmings have been down to takeover approaches, where I have trimmed at least once before the final disposal.

The movements are often fairly rapid, and contrary to the market. You cannot predict them, and often it comes to nothing. It makes life interesting.

TJH

Re: Selling Unilever?

Posted: September 13th, 2019, 11:02 pm

by Gengulphus

Spet0789 wrote:Why not just sell 2% every year if you want the income?

Hey presto, a 5% income yield and I suspect the total return would still outperform a few of the usual suspects with ‘natural’ 5% yields.

Perfectly reasonable answer -

if your holding is big enough for selling 2% of it to be a cost-effective sale

and you've got the self-discipline to just get on with it each year without worrying endlessly about whether you're doing the right thing

and you don't mind the fact that selling 2% of your holding will produce an amount of 'income' that is sometimes 'cut'. Such 'cuts' are produced by the stockmarket rather than company directors, and the stockmarket tends to make significantly more volatile decisions about 'cutting' than company directors,

Gengulphus

Re: Selling Unilever?

Posted: September 13th, 2019, 11:18 pm

by Alaric

Gengulphus wrote:Perfectly reasonable answer - if your holding is big enough for selling 2% of it to be a cost-effective sale

You might do it at a portfolio level. Suppose you were getting a running yield of 3% with price and dividend growth of around 6%. If you need an extra 2% to pay the bills, you sell something. Higher risk to the income stream than locking in at 5% and no growth, but higher reward. It could make sense to have the "something" you sell as an IT, so as not to unbalance.

Re: Selling Unilever?

Posted: September 13th, 2019, 11:20 pm

by Lootman

Gengulphus wrote:Spet0789 wrote:Why not just sell 2% every year if you want the income?

Hey presto, a 5% income yield and I suspect the total return would still outperform a few of the usual suspects with ‘natural’ 5% yields.

Perfectly reasonable answer -

if your holding is big enough for selling 2% of it to be a cost-effective sale

and you've got the self-discipline to just get on with it each year without worrying endlessly about whether you're doing the right thing

and you don't mind the fact that selling 2% of your holding will produce an amount of 'income' that is sometimes 'cut'. Such 'cuts' are produced by the stockmarket rather than company directors, and the stockmarket tends to make significantly more volatile decisions about 'cutting' than company directors,

I think the point that Spet0789 makes is valid. What ultimately matters is that the annual rate of withdrawal (whether in dividends or in capital) is lower than the long-term average expected annual total return. As long as that is the case then it doesn't matter whether that withdrawal is funded by dividends, capital or a mix of the two.

That said, it is obviously ideal if your annual cashflow needs can be met purely from dividends. But then you might as well say it is better to be richer so that that is possible, and that may not be helpful. But the reality remains that there is a significant class of people for whom it is true that they cannot fund retirement merely from dividends, but they can if they also draw down capital. And this is particularly relevant for those who do not have as an investment objective the desire to pass wealth onto others upon their death.

The way I think of it is this. We naturally divide into three groups:

1) Those with sufficient wealth that they can live off only the dividends

2) Those who are so broke they can never retire at all

3) Those in between who can't live only off their dividends but can live off a mix of dividends and capital drawdown.

It is the class of people in (3) for whom Spet's drawdown idea makes sense, and especially if invested in more defensive, less volatile names like Unilever rather than high yielders with their elevated risk profile.

Re: Selling Unilever?

Posted: September 14th, 2019, 9:16 am

by scrumpyjack

Logically, Lootman, you are of course quite right. But there is also a psychological dimension to this. The distinction, perhaps rather illogical, between capital and income. Many people prefer not to feel they are eroding their ‘capital’ but are living off ‘income’. Hence they prefer high yielding shares, with poorer prospects, to lower immediate yield shares with better prospects.

Re: Selling Unilever?

Posted: September 14th, 2019, 11:54 am

by Itsallaguess

scrumpyjack wrote:

Many people prefer not to feel they are eroding their ‘capital’ but are living off ‘income’.

Hence they prefer high yielding shares, with poorer prospects, to lower immediate yield shares with better prospects.

It's clear that there are many ways to skin a cat with regards to living off investments, but we should be careful to remember that whilst there might be general agreement that companies like Unilever exist, who tend to display a relatively lower-yielding distribution but also display long-term total-return benefits, it's not

just a case of simply moving down the yield list and expecting every company to show such solid, multi-year growth....

There's poor investments all over the yield list, whether they be in high-yield territory or lower-yield territory, so it's not just a case that altering our approach to that single metric is going to deliver automatically good returns...

Where are all these '

lower immediate-yield shares with better prospects'?

This thread might be about one of them, but where's the rest of the 'portfolio'?

I should add that I ask this as an advocate of lower-yielding (compared to many HYP shares...) Investment Trusts, so I'm quite happy to accept lower-yielding investments as part of my approach, although I don't expect too much regarding the 'total return' aspect of my income-IT holdings...

Cheers,

Itsallaguess

Re: Selling Unilever?

Posted: September 14th, 2019, 12:06 pm

by Alaric

Itsallaguess wrote:

There's poor investments all over the yield list, whether they be in high-yield territory or lower-yield territory, so it's not just a case that altering our approach to that single metric is going to deliver automatically good returns...

The "high yield only" approach excludes a lot of decent stuff. Or at least it does now, maybe twenty years ago it didn't as then there were any number of "tech boom" companies around with share prices at a multiple of several times what they were objectively worth in the sense of their ability to make and distribute profits.

Re: Selling Unilever?

Posted: September 14th, 2019, 12:17 pm

by Spet0789

If you adhere to the Munger / Train / Smith view, which I do, the only thing that matters is the long run ability of a company to earn high returns on capital.

If (1) the company can reinvest profits and compound those returns and (2) the price/book value of the company remains relatively stable over time, then investing in those companies will always deliver more ‘income’ via a systematic selldown strategy.

At the risk of being controversial, the HYP approach is to operationally easier (you just sit there and the portfolio throws off cash) and emotionally simpler as it doesn’t feel like the portfolio is being sold down. But it is probably destined to underperform as it deliberately ignores return on capital considerations. In fact, companies with low return on capital or inability to efficiently deploy capital are perhaps more likely to pay high dividends, leading to an underperformance of HYP shares vs the market.

None of this detracts from the fact that a HYP is, in my view, better than an annuity at today’s levels of rates and that’s what it was designed to replace.

Re: Selling Unilever?

Posted: September 14th, 2019, 12:36 pm

by Dod101

We tend to forget that the HYP was designed for a Doris, who almost be definition is not going to be looking at her portfolio every week or even every month. She just takes the income and is happy to have it. In many ways I cannot help thinking that that is the best way to treat a HYP. Just leave it alone. It was though also designed in a different investing environment. Today many of its expected characteristics seem also to have gone out of the window so that we have what seem to be good companies freezing their dividends (HSBC, Shell and the two pharmas for starters). We have other companies where the dividend is still increasing and yet the share price is virtually unmoved`; hence the high yields on shares like Legal and general, the tobaccos and so on.

On the subject of living off capital, I would feel most uncomfortable doing that as part of my regular income because the stock market goes down as well as up as we all know. I am prepared to use capital for a significant one off capital expenditure because I can then time my sale to suit or at least time it to satisfy my judgement of the state of the market. Obviously I cannot do that if I need a capital sale for monthly income.

Dod

Re: Selling Unilever?

Posted: September 14th, 2019, 1:01 pm

by Spet0789

Dod101 wrote:We tend to forget that the HYP was designed for a Doris, who almost be definition is not going to be looking at her portfolio every week or even every month. She just takes the income and is happy to have it. In many ways I cannot help thinking that that is the best way to treat a HYP. Just leave it alone. It was though also designed in a different investing environment. Today many of its expected characteristics seem also to have gone out of the window so that we have what seem to be good companies freezing their dividends (HSBC, Shell and the two pharmas for starters). We have other companies where the dividend is still increasing and yet the share price is virtually unmoved`; hence the high yields on shares like Legal and general, the tobaccos and so on.

On the subject of living off capital, I would feel most uncomfortable doing that as part of my regular income because the stock market goes down as well as up as we all know. I am prepared to use capital for a significant one off capital expenditure because I can then time my sale to suit or at least time it to satisfy my judgement of the state of the market. Obviously I cannot do that if I need a capital sale for monthly income.

Dod

If you systematically sell 1% of your portfolio for income every quarter, you’re not timing the market, any more than if you make monthly savings. It puts you no more at risk of stock market fluctuations than taking a dividend rather than reinvesting it. But it feels different and that’s why many of those who haven’t thought about the maths (as I have) are uncomfortable with it.

Dividend income is more stable, but ultimately it all comes from the same pot. I think anyone drawing income from an equity portfolio should be willing to adjust their spending as market returns change.