BP and Shell

Posted: January 16th, 2022, 1:37 pm

Afternoon all,

I was reading:https://www.common-wealth.co.uk/reports/drilling-down#chapter-2 There is obviously a political argument behind the paper, so interpretations of their conclusions will vary! However they do present some data for FTSE 100 averages, as well as BP and Shell, for 2010-20.

The appendix includes FTSE 100 data (total 2010-20) which shows an average £15.9 billion in pre-tax income, of which: £5 billion went in income taxes; £8.2 billion in dividends; and £2.6 billion in share buybacks.

BP data on the same basis has an average £52 billion in pre-tax income, of which £20.2 billion went in income taxes; £42.6 billion in dividends; and £8.5 billion in share buybacks.

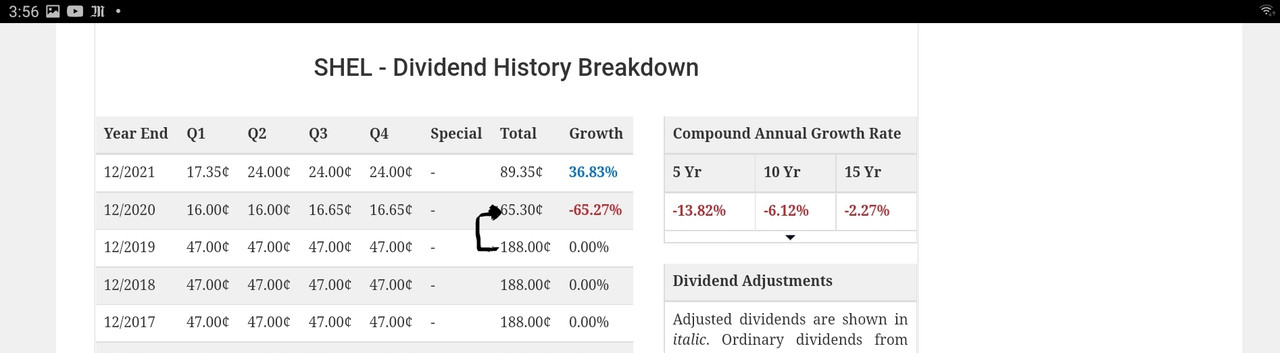

Shell data has £173.4 billion in pre-tax income, of which £74.7 billion went in income taxes; £76.7 billion on dividends; and £19.4 billion in share buybacks.

The extent to which individual companies are paying a large proportion of their income as dividends (or more than their income as dividends) is a key consideration for dividend sustainability. Are they able to sustain dividend payments if they are devoting a smaller proportion of their income to investing in future growth?

Disclosure: Held Shell 1998-2010; held BP 1998-2015.

Best wishes

Mark.

I was reading:https://www.common-wealth.co.uk/reports/drilling-down#chapter-2 There is obviously a political argument behind the paper, so interpretations of their conclusions will vary! However they do present some data for FTSE 100 averages, as well as BP and Shell, for 2010-20.

The appendix includes FTSE 100 data (total 2010-20) which shows an average £15.9 billion in pre-tax income, of which: £5 billion went in income taxes; £8.2 billion in dividends; and £2.6 billion in share buybacks.

BP data on the same basis has an average £52 billion in pre-tax income, of which £20.2 billion went in income taxes; £42.6 billion in dividends; and £8.5 billion in share buybacks.

Shell data has £173.4 billion in pre-tax income, of which £74.7 billion went in income taxes; £76.7 billion on dividends; and £19.4 billion in share buybacks.

The extent to which individual companies are paying a large proportion of their income as dividends (or more than their income as dividends) is a key consideration for dividend sustainability. Are they able to sustain dividend payments if they are devoting a smaller proportion of their income to investing in future growth?

Disclosure: Held Shell 1998-2010; held BP 1998-2015.

Best wishes

Mark.