Bubblesofearth wrote:Gold, like property, is a real asset. Cash, bonds and equities are financial assets. I am increasingly of the opinion that holding a mix of both real and financial assets is a good idea.

Don't forget currencies. If you historically stuffed equal values of US$ and gold under your mattress then that alone offset a significant amount of UK inflation. Since 1896, all but -0.6% (assuming T-Bills were held pre 1932 ending of gold/money convertibility as that was like holding gold that paid interest).

Modern day ancient Talmud style (thirds each land, business, in-hand advice) ...

Initial third in a UK house, has imputed rent benefit and house+imputed is similar to stock+dividends.

A third in US$, primary reserve fiat currency, invested equally in BRK and MKL that pay no dividends.

A third in physical gold, legal tender coins (tax exempt).

Collectively like a 67/33 equity/gold asset allocation. Broadly if you held gold or bonds outcomes tended to be much the same, at least in gross terms, after taxation of bond interest however !!!

Once loaded, no further rebalancing, just draw a 3% SWR from the stock/gold assets, whichever is the higher value of the two at the time. Which is a form of partial rebalancing.

Historic outcomes whether you yearly rebalanced back to target weighting, or just left as-is (with withdrawals from the most above target weighting, or additions/savings added to the most below target weighting), tended to broadly compare, similar 30 year final values either way. Coin flip as to whichever was the better.

Tax return report ... income 0%. Capital gain may be payable on the SWR amount if some stocks are sold, reduced by yearly CGT allowance, or exempt if held inside a ISA.

Currency diversification of £, and US$ fiat currencies, global non-fiat currency (gold).

Asset diversification of land, stocks, commodity.

Counter-party risk is just the initial third in stocks, land (home) and gold (physical) are in-hand, zero counter-party risk.

Time to cash in-hand, T+3. But perhaps more like a 4 day notice account in practice i.e. three days to sell some shares and have the sale proceeds added to your account, and another day to transfer the cash to your regular bank/spending account. In the case of liquidating gold, more often you can do that the same day, at least for smaller amounts such as one or two Britannia one ounce gold coins sold to a local dealer (for around £3K of cash at recent prices).

The 3% SWR above = 2% relative to total wealth. Supplemented with imputed rent benefit, the rent you'd otherwise have to find/pay. Historically 4.2%, so 1.4% proportioned to a third of total wealth. Combined 2% + 1.4% = 3.4%. SWR observations are typically measured across 30 year periods, so in effect 3.33% x 30 years = the return of your inflation adjusted capital via 30 yearly instalments. If you start with all of your capital at risk, have half having been returned after 15 years (via SWR), all returned after 30 years, then average capital at risk = 50%. Typically the above ended 30 years with your inflation adjusted wealth still also intact, so 2x total return. ( 2 / 0.5 )^(1/30) = 1.0473 = 4.73% annualised real rate of return on average capital at risk.

Take your SWR monthly, and its just a case of selling some gold, or some shares to provide your regular inflation adjusted 'wage'. Beyond that no other actions are required.

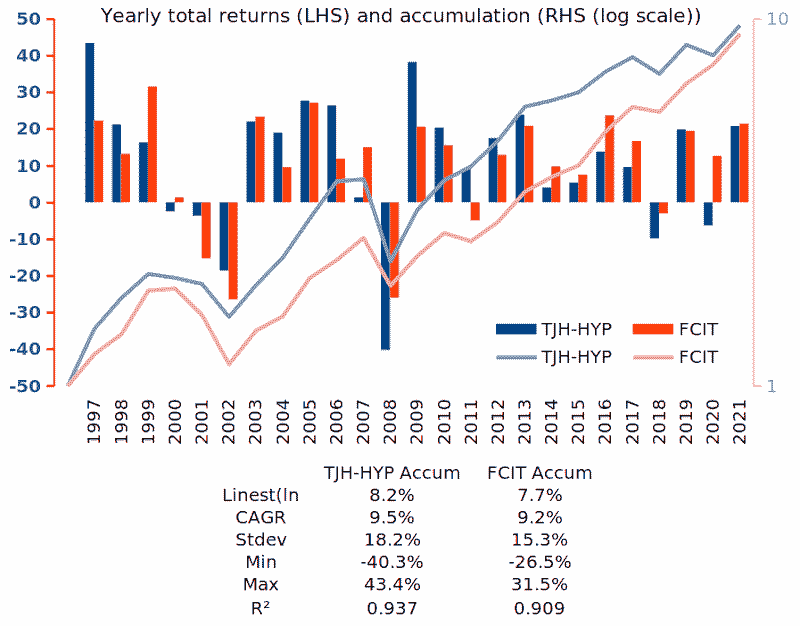

Historic prices ...

A no tinker No Yield Portfolio (NYP). Where 25/25/50 BRK/MKL/Gold in 2022 resulted in a +15% gain. And where you define how much and when DIY dividends are paid out.