Urbandreamer wrote:1nvest wrote:

Why store/hold/invest in £50 and £20 notes when alternative "currencies" such as US stock share certificates and gold can also relatively quickly/easily be converted into £10/£5 notes for local 'bartering' purposes.

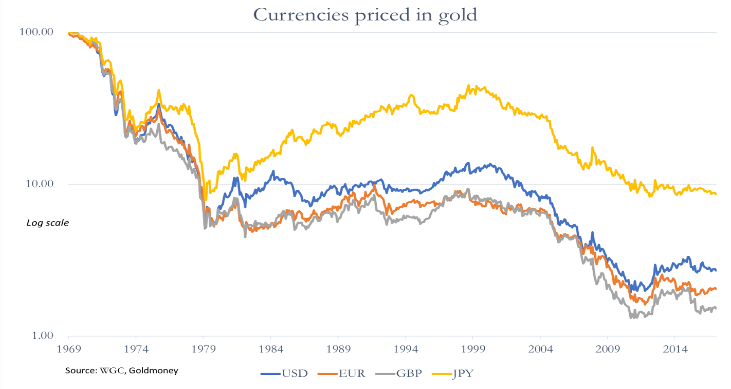

Ignoring the political point's about specific countries governments, that's a interesting chart.

As it happens the IC has a interesting article about the purchasing power of gold.

https://www.investorschronicle.co.uk/ne ... as-soared/Personally I think that it says a lot more about the fiat currency system, than the economy. If it does say anything about the economy then what it says is either that gold is getting more scarce or that we are finding ways of reducing the marginal cost of production.

Ps, off topic for this board, but I'm seriously considering changing the currency that I use. Now that we use contactless debit cards this is actually an option.

(e)wallet 'currency' of US stock accumulation fund certificates and gold in equal value measure (yearly rebalanced), 1896 to recent log linear regression slope measures (general trend line) and that 'currency' saw other 'assets' historic price decline rates of ....

Consumer prices -4.8%

House Prices -2.7% annualised

Pound currency (hard cash) -9.1%

UK stock (price only) -4.2%

US stocks (price only) -2.6%

Cash deposit (T-Bills) -3.7%

Of course that 'currency' is 'foreign', you can't walk into a grocery store and pay in a US S&P500 stock index share, has to be converted to Pounds first, as with any other currency. Typically a T+2 days conversion notice/time. Alternatively pay by credit card, and do the conversion a few days prior to paying off that months credit card bill.

Alongside owning a UK home (GB£), that's additionally US$ fiat currency and non-fiat commodity currency (gold), asset diversity of land, stocks, commodity.

Commonly however and many prefer to measure relativity based to hard cash Pounds, which historically at least where the worst currency to keep in your wallet.

A note about rebalancing, that just reduces concentration risk, doesn't broadly add to rewards (introduces additional costs). If you don't rebalance for a decade then 50/50 will tend to end up with a high weighting in the more productive/rewarding asset(s), may end up at 80/20 ... such that you time-averaged 65/35 in the best/worst assets. Rebalancing is inclined to yield a comparable reward to that (on average, but different time periods may see that swing either way), but where you were less concentrated into a single asset, more consistently remained at around 50/50 exposure levels. Additions/withdrawals applied to a non-rebalanced portfolio can be directed in a manner where that is a form of partial rebalancing, add to the most-down, draw from the most-up. i.e. if your (e)wallet contents stock value is greater than the wallets gold contents value, then spend stock certificates (otherwise spend gold). Which simplifies things, such as for heirs. Load up 50/50 at retirement, spend down whichever is the higher value each month in order to pay off the credit card bill, beyond which there's no other management required (no yearly rebalance trades involved). A exception however is if the two values become considerably different, such as if the weightings had increased to/above 75/25 when the concentration risk might be considered a bit too high.

Working in your favour is that the UK will take steps to prop-up/maintain its housing market, as will the US take steps to prop-up/maintain its stock markets, so you're aligned with "don't fight the fed".