1. Current CAPE SP500 is 39.2. Historical average 15.8.

https://www.multpl.com/shiller-pe2. Current PER SP500 estimated at 29, historical average around 15.

https://www.multpl.com/s-p-500-pe-ratio3. Current price/sales SP500 is 3.15x. Long term 1.5x.

4. [1-3] all suggest that if the market were to mean-revert right now the SP500 would lose 50% in real terms.

5. If the SP500 were to overshoot the mean to historical lows, we'd be looking at 80%+ drop in real terms.

6. Buffett ratio of total US market cap vs GDP at 213%, vs historical trend of 120%, i.e. 71% overvalued. Implying 44% drop to mean revert.

7. Household stockmarket holdings as % of portfolios is now equal to all time high of the dotcom era.

https://fred.stlouisfed.org/graph/?g=qis 8. 2-year government debt in Australia spiked from 0.1% to 0.8%

in just one day last week, after the central bank decided not to defend against the market movement. Yikes. Potentially a big impact on fixed rate mortgages, short-term company debt costs if it doesn't drop back, or if we see this in other debt markets.

9. Property & construction are about 30% of the Chinese economy and are looking into a bad debt tsunami and new property tax. May impact some UK companies - HSBC, Standard Chartered, miners? May broadly impact world economy. Multiple large chinese property developers have defaulted on some debt or missed payments and are in pre-default.

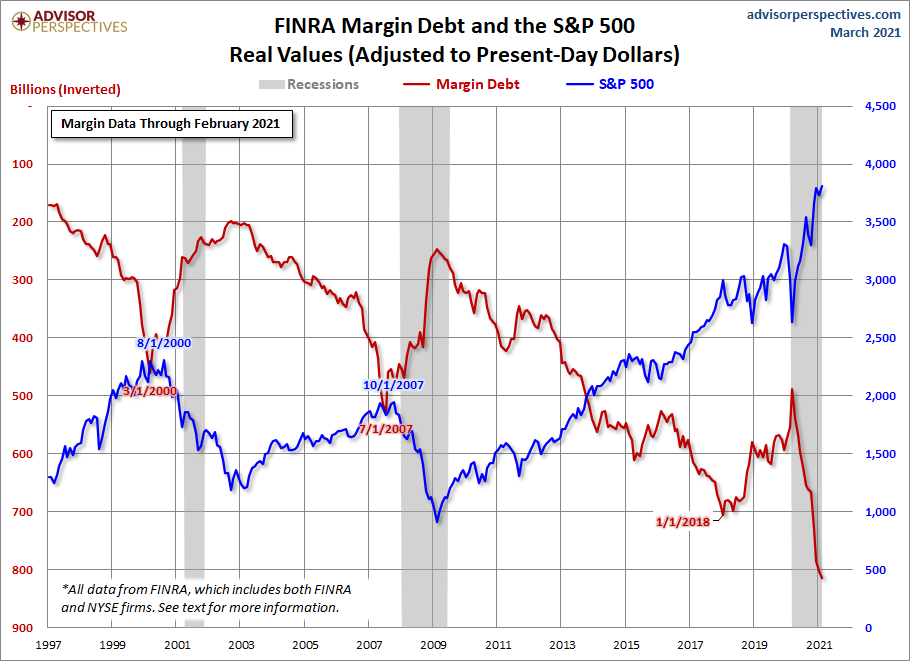

10. Use of margin debt vs SP500 level is now at an all-time record high far above any past mania or bubble. This does not include growth in use of options which I understand to be very high and often combined with margin (and I'm told, funded by a credit card.... smh). Note that this metric is measured against the SP500 which itself is already at an all-time high. If you measure against something more stable during bubbles - e.g. GDP, or aggregate sales of the SP500 - this figure for use of margin will look completely off-the-chart insane. Finally note this chart is dated for September and the market has zoomed up even higher since then.

https://www.advisorperspectives.com/ima ... 59a77b.png11. Economic backdrop. Companies facing margin pressure from labour costs, corporation tax rising globally, logistics costs, input prices rising, energy costs, long-term interest rate costs starting to rise, difficulty trading generally (staff sick/isolating, logistics difficulties getting parts, selling outputs). Tax on individuals is also rising at the same time as e.g. long-term mortgage rates and general inflation. Inflation has generally been bad for stock price growth in real terms.

12. Fear and Greed index:

https://money.cnn.com/data/fear-and-greed/72/100: GREED. Showing 'extreme greed' and risk-taking on many metrics.

13. Greed & mania in individual stocks is widespread in the SP500.

https://finviz.com/map.ashx?t=sec&st=pehttps://finviz.com/map.ashx?t=sec&st=ps14. TSLA price to earnings ratio around 360x. Eh. WTF.

WTF!15. Global logistics chaos and 10-20x higher costs not expected to clear until 2023.

16. Interest rate decisions this week from various central banks, talk of moving forward rate rises and tapering by many months from late 2022/2023 into 2021 or early 2022. Previous discontinuances of QE (tapering) has led to 'taper tantrum' stockmarket corrections.

17. Stimulus program in the USA to be far, far smaller than originally proposed.

18. Yield curve is flattening, yield curve inversion historically predicts recession. 20y treasury yield already inverted above 30y. (

https://www.bloomberg.com/news/articles ... year-bonds)

Right now, it feels good to be mostly in short-term (1-3 year) government bonds.

Best of luck to those 100% long in the market, you will probably need it.

comp

{kind=link}

{kind=link}