Page 2 of 3

Re: What's in your portfolio and why?

Posted: October 4th, 2021, 5:28 pm

by Aminatidi

Very boring this lot is about £270K last time I looked (easier not to right now

)

Stock name % Weight Sector

1 Fundsmith Equity Class I 29.8% Global -

Hopefully continues its pattern of solid steady growth with no surprises.2 Ruffer Investment Company Red Ptg Pref Shs GBP0.0001 28.7% [N/A] -

Made a tidy profit off this and haven't quite got around to working out if it's a keep - hoping it will come in handy if the brown stuff properly hits the fan.3 Capital Gearing Trust Plc Ord GBP0.25 20.7% [N/A] -

Does what it says on the tin and I wouldn't have a hope in hell of playing the discount game the way they do.4 UK Buffettology General 10.7% UK All Companies -

Hopefully continues its pattern of solid steady growth with no surprises.5 Smithson Investment Trust Plc Ord GBP 10.0% [N/A] -

Hopefully continues its pattern of solid steady growth with no surprises.6 Cash 0.1% [N/A]

I guess I'm trying to "barbell" between growth and preservation with hopefully minimal volatility along the way whilst accepting there has to be

some in order to accumulate.

Re: What's in your portfolio and why?

Posted: October 4th, 2021, 6:58 pm

by absolutezero

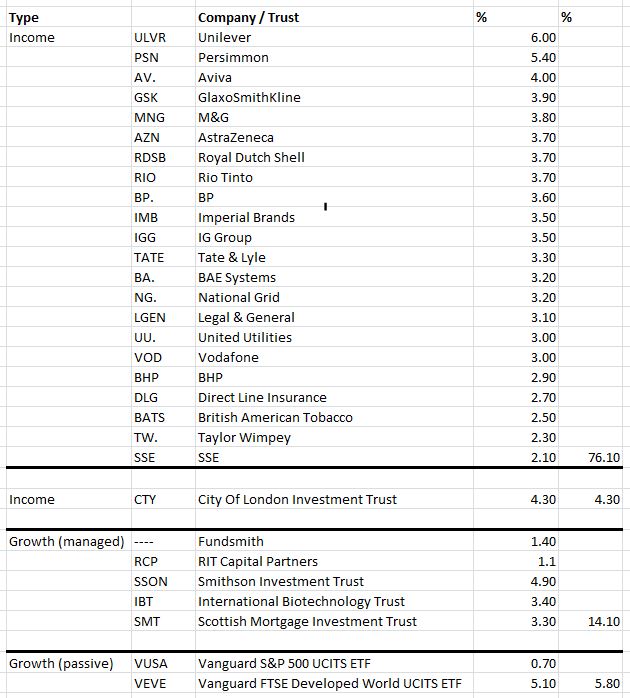

monabri wrote:I've re-arranged the cards. The portfolio is income focussed (80%) with growth elements (20%) - numbers don't tally to 100% (close) but that's because of rounding in the original presentation.

The question for me would be, where do I concentrate on next - carry on increasing the income bearers (perhaps adding international ITs such as MYI) or growth? If "growth", would one adopt passive investment or active ?

edit: I guess that this is what Dod is saying.

I did also think about organising the table like this.

If you had asked I would have done that for you! But thank you.

With regard to your question. International + growth. I have enough income.

That's not to say some of the income shares won't grow. They will, though some will likely be dogs as well.

And a mixture of active ITs + some passive trackers.

Re: What's in your portfolio and why?

Posted: October 4th, 2021, 7:02 pm

by absolutezero

77ss wrote:Looking at your holdings, I would be much more inclined to trim ULVR. I hold this (2.6%), but am starting to wonder whether it is worth the candle.

Never fall in love with a share, but if someone said to me you have to liquidate your entire portfolio and can only hold one share, that share would be Unilever.

If they said an IT then my answer would probably be Scottish Mortgage or RIT.

Re: What's in your portfolio and why?

Posted: October 5th, 2021, 8:58 am

by moorfield

absolutezero wrote:77ss wrote:Looking at your holdings, I would be much more inclined to trim ULVR. I hold this (2.6%), but am starting to wonder whether it is worth the candle.

Never fall in love with a share, but if someone said to me you have to liquidate your entire portfolio and can only hold one share, that share would be Unilever.

If they said an IT then my answer would probably be Scottish Mortgage or RIT.

I wouldn't hold an individual company, but am interested in holding a single collective IT to replace an (sort of) HYP - but which? CTY or MRCH perhaps. What I suspect I may gravitate towards is holding one IT each from a different AIC sector per the list that IAAG recently posted.

Re: What's in your portfolio and why?

Posted: October 5th, 2021, 10:54 am

by Newroad

Hi AbsoluteZero.

SMIT and RIT are interesting (and in my opinion, questionable) single trust choices.

However together, with some sort of (say) annual rebalance, they provide an interesting barbell option - so I wouldn't mind holding just the two of them 50% each.

Regards, Newroad

Re: What's in your portfolio and why?

Posted: October 5th, 2021, 11:02 am

by tjh290633

Another factor that I keep an eye on is the change in share price from 1st January to date. As at last night, my portfolio has shown these changes:

Epic Change Yield

IMI 40.00% 1.40%

S32 35.60% 2.65%

BP. 35.18% 4.46%

MKS 34.89% 0.00%

RDSB 32.67% 3.24%

SGRO 25.37% 1.90%

LLOY 22.94% 2.77%

DGE 22.29% 2.06%

AV. 21.40% 5.41%

KGF 21.01% 2.84%

AZN 20.51% 2.29%

BA. 15.38% 4.29%

BT.A 14.52% 5.08%

CPG 11.23% 0.00%

UU. 9.23% 4.42%

TSCO 8.75% 3.64%

ADM 7.60% 7.90%

SMDS 7.53% 3.00%

PSON 5.53% 2.76%

LGEN 4.62% 6.40%

SSE 4.50% 5.14%

NG. 4.38% 5.44%

GSK 3.19% 5.78%

MARS 3.17% 0.00%

IMB 1.40% 8.87%

TATE 1.13% 4.52%

PHP -0.46% 4.08%

BLND -0.51% 3.09%

BHP -3.97% 11.76%

VOD -5.08% 6.81%

BATS -5.21% 8.40%

IGG -6.55% 5.36%

TW. -7.90% 5.42%

ULVR -10.10% 3.78%

RIO -12.02% 14.39%

RKT -13.54% 3.09%

Av.Chg 9.69% 4.51%

If you look at my earlier post

viewtopic.php?p=447797#p447797 you will see some familiar names at the top of the list from both lists that I posted.

TJH

Re: What's in your portfolio and why?

Posted: October 6th, 2021, 3:59 pm

by Humeau

Cash

Philip Morris

Facebook

Amadeus

Smartsheet

Adobe

Prosus

Qualys

Mastercard

Unilever

Zoetis

Sabre Corp

Fundsmith

Alphabet A

I like long term compounders with high ROIC, margins and reinvestment possibilities.

Re: What's in your portfolio and why?

Posted: October 6th, 2021, 7:13 pm

by BT63

1. Cash: 13%

2. Gold: 26%

3. High yield shares: 45%

4. OEIC/UT/ETF/IT & Other: 16%

Why?

1. Because I don't think there's much value out there, so not all available money is being reinvested.

2. In case the excrement hits the fan after the distortions of QEternity.

3. I live off part of the income they generate.

4. Because I'm getting lazy and can't be bothered trying to find/research/analyse high yielders for my portfolio, so have only been adding to OEIC/UT/ETF/IT etc in the last several years.

Re: What's in your portfolio and why?

Posted: October 6th, 2021, 7:49 pm

by absolutezero

BT63 wrote:1. Cash: 13%

2. Gold: 26%

3. High yield shares: 45%

4. OEIC/UT/ETF/IT & Other: 16%

Why?

1. Because I don't think there's much value out there, so not all available money is being reinvested.

2. In case the excrement hits the fan after the distortions of QEternity.

3. I live off part of the income they generate.

4. Because I'm getting lazy and can't be bothered trying to find/research/analyse high yielders for my portfolio, so have only been adding to OEIC/UT/ETF/IT etc in the last several years.

What individual shares do you hold in your high yield shares and OEIC/IT sections?

Re: What's in your portfolio and why?

Posted: October 6th, 2021, 8:16 pm

by BT63

absolutezero wrote:BT63 wrote:1. Cash: 13%

2. Gold: 26%

3. High yield shares: 45%

4. OEIC/UT/ETF/IT & Other: 16%

Why?

1. Because I don't think there's much value out there, so not all available money is being reinvested.

2. In case the excrement hits the fan after the distortions of QEternity.

3. I live off part of the income they generate.

4. Because I'm getting lazy and can't be bothered trying to find/research/analyse high yielders for my portfolio, so have only been adding to OEIC/UT/ETF/IT etc in the last several years.

What individual shares do you hold in your high yield shares and OEIC/IT sections?

I have quite a lot of holdings but the largest are companies which I felt had dividend-paying resilience when I bought them many years ago, and amazingly most of them kept paying a decent dividend through Covid!

Largest shareholdings (each is ~5% of whole portfolio and ~10% of the high-yield part):

AstraZeneca

GlaxoSmithKline

SSE

National Grid

Sainsbury's

Imperial Brands

Tesco

Of the UT/IT/OEIC/ETF type of investments, my main interest in recent years has been accumulating UK mid caps including HSBC FTSE 250 OEIC and L&G FTSE 250 OEIC, each rivalling one of my larger dividend-paying shareholdings listed above.

I have some international exposure but reduced much of that some months ago - especially US - and reinvested the proceeds into UK midcaps.

Re: What's in your portfolio and why?

Posted: October 7th, 2021, 2:12 pm

by 1nvest

£, $, global currencies diversity, land, stocks, commodity asset diversity, looking to a third of each.

Each have their good and bad 20 (30) year times, and I don't want to be holding/relying-upon just the single worst case alone (concentration risk). Average out historic stock performance, account for costs/taxation and discount true inflation (not the understated inflation that is used by the state to lower the likes of pension/wage increases that otherwise would have to be paid) - and stocks aren't always the panacea that many opine them to be.

£ in UK home, mitigates (liability matches otherwise) having to find/pay rent.

$ in US stock, heart of capitalism with a large land mass/resources

Gold global currency (and a commodity) or silver.

Rebalancing is largely optional, but non-rebalanced can at times see considerable drift in weightings having occurred, so never say never.

In drawdown/retirement so SWR with ratchet (each year revise to : inflation uplifted SW value or SWR %, whichever is the higher) yields the more consistent inflation pacing/beating income. Historically 2% SWR was safe, that excludes imputed rent benefit, of the order 3.5% benefit including imputed rent benefit ... which is relative to total wealth. proportioned to just liquid assets = 5.25%. Similar to all-stock alone average case, but where the historic worst cases were diluted down significantly (near totally mitigated), but at the expense of all-stock best/better case outcomes being considerably more better (more concerned about getting through life comfortably over that of having the most expensive tombstone in the graveyard).

Re: What's in your portfolio and why?

Posted: October 8th, 2021, 8:28 pm

by absolutezero

BT63 wrote:absolutezero wrote:BT63 wrote:1. Cash: 13%

2. Gold: 26%

3. High yield shares: 45%

4. OEIC/UT/ETF/IT & Other: 16%

Why?

1. Because I don't think there's much value out there, so not all available money is being reinvested.

2. In case the excrement hits the fan after the distortions of QEternity.

3. I live off part of the income they generate.

4. Because I'm getting lazy and can't be bothered trying to find/research/analyse high yielders for my portfolio, so have only been adding to OEIC/UT/ETF/IT etc in the last several years.

What individual shares do you hold in your high yield shares and OEIC/IT sections?

I have quite a lot of holdings but the largest are companies which I felt had dividend-paying resilience when I bought them many years ago, and amazingly most of them kept paying a decent dividend through Covid!

Largest shareholdings (each is ~5% of whole portfolio and ~10% of the high-yield part):

AstraZeneca

GlaxoSmithKline

SSE

National Grid

Sainsbury's

Imperial Brands

Tesco

Of the UT/IT/OEIC/ETF type of investments, my main interest in recent years has been accumulating UK mid caps including HSBC FTSE 250 OEIC and L&G FTSE 250 OEIC, each rivalling one of my larger dividend-paying shareholdings listed above.

I have some international exposure but reduced much of that some months ago - especially US - and reinvested the proceeds into UK midcaps.

The general wisdom is that ETFs are cheaper than OEICs.

I'd be interested why you use FTSE250 OEICs instead of ETFs.

Re: What's in your portfolio and why?

Posted: October 8th, 2021, 9:15 pm

by vagrantbrain

No individual shareholdings for me after a few years realising i'm not Peter Lynch, nor do I have the energy to try to be. Looking for long term growth with 25+ years working life left. Cheap global trackers make up about 60% and rising which i'm intending to hold for the long term, the others may be more transient depending on my educated guesses as to the market trends.

1) Allianz Technology Trust (ATT), 12.7% - IMHO significant gains to be made in the next decades from cloud/SAAS but I lack industry knowledge

2) Vanguard FTSE all-world tracker (VWRL), 21.4% - I'm unlikely to beat the market so bought the market

3) Schroder Asia Pacific (SDP), 8.7% - Too much dodgy activity in the region for meto trust a tracker, rather pay someone to hopefully avoid the obvious traps

4) NASDAQ tracker (EQQQ), 1.3% - Recent purchase - cheaper and less volatile then ATT

5) Scottish Mortgage Trust (SMT), 15.5% - Proven track record with growth companies

6) HSBC MSCI developed world tracker (HMWO), 36.3% - First tracker I purchased after realising I was unlikely to beat the market

7) Autoenrollment DC pension, 4.0% - Bit of a dog and unable to change fund choices but I get employer contributions

Re: What's in your portfolio and why?

Posted: October 8th, 2021, 9:19 pm

by BT63

absolutezero wrote:The general wisdom is that ETFs are cheaper than OEICs.

I'd be interested why you use FTSE250 OEICs instead of ETFs.

No complex logic - just old habits.

Re: What's in your portfolio and why?

Posted: October 10th, 2021, 9:12 am

by YeeWo

absolutezero wrote:Never fall in love with a share, but if someone said to me you have to liquidate your entire portfolio and can only hold one share, that share would be Unilever.

I've held Unilever since 2011 and really like this business too. It does seem though that the SP really hasn't recovered from C19, activists are being mentioned. The Unilever Indonesia Tbk shareprice is back at 2013 levels. A sum of parts valuation has the business circa 25% undervalued. If you've held Unilever for some time and you believe in the longer term narrative,

Now might be a damned good time to top-up your investment........

Re: What's in your portfolio and why?

Posted: October 10th, 2021, 1:35 pm

by absolutezero

YeeWo wrote:absolutezero wrote:Never fall in love with a share, but if someone said to me you have to liquidate your entire portfolio and can only hold one share, that share would be Unilever.

I've held Unilever since 2011 and really like this business too. It does seem though that the SP really hasn't recovered from C19, activists are being mentioned. The Unilever Indonesia Tbk shareprice is back at 2013 levels. A sum of parts valuation has the business circa 25% undervalued. If you've held Unilever for some time and you believe in the longer term narrative,

Now might be a damned good time to top-up your investment........

ULVR did home into view with its dividend yield climbing high enough to (just about) trigger the HYP lot buying.

ULVR is a quality company. You pay for quality.

Re: What's in your portfolio and why?

Posted: October 10th, 2021, 1:38 pm

by absolutezero

vagrantbrain wrote:No individual shareholdings for me after a few years realising i'm not Peter Lynch, nor do I have the energy to try to be. Looking for long term growth with 25+ years working life left. Cheap global trackers make up about 60% and rising which i'm intending to hold for the long term, the others may be more transient depending on my educated guesses as to the market trends.

1) Allianz Technology Trust (ATT), 12.7% - IMHO significant gains to be made in the next decades from cloud/SAAS but I lack industry knowledge

2) Vanguard FTSE all-world tracker (VWRL), 21.4% - I'm unlikely to beat the market so bought the market

3) Schroder Asia Pacific (SDP), 8.7% - Too much dodgy activity in the region for meto trust a tracker, rather pay someone to hopefully avoid the obvious traps

4) NASDAQ tracker (EQQQ), 1.3% - Recent purchase - cheaper and less volatile then ATT

5) Scottish Mortgage Trust (SMT), 15.5% - Proven track record with growth companies

6) HSBC MSCI developed world tracker (HMWO), 36.3% - First tracker I purchased after realising I was unlikely to beat the market

7) Autoenrollment DC pension, 4.0% - Bit of a dog and unable to change fund choices but I get employer contributions

I'm in the middle of reading 'Smarter Investing' by Tim Hale.

He cites a lot of evidence showing the active managers (with one or two exceptions) are not able to consistently beat the market.

He then says the problem with the exceptions is identifying them early on.

For him, he insists that cheap trackers are the best way for normal people to buy shares.

Re: What's in your portfolio and why?

Posted: October 14th, 2021, 9:45 am

by Hariseldon58

absolutezero wrote:BT63 wrote:absolutezero wrote:What individual shares do you hold in your high yield shares and OEIC/IT sections?

The general wisdom is that ETFs are cheaper than OEICs.

I'd be interested why you use FTSE250 OEICs instead of ETFs.

Whilst not directed at me I do hold some OEICs,( far more ETFs)

Track an index not otherwise available as ETF, eg Vanguard Total US Market.

More established than the ETF equivalent eg Vanguard World Small Cap, more holdings, ie better representation, cheaper than the ETF equivalent.

Diversification of product type, in the event of a market failure, company failure, fraud etc

Invariably an accumulation version is available.

Clearly there are active OEICs without an ETF equivalent, may have an IT alternative though.

Re: What's in your portfolio and why?

Posted: October 14th, 2021, 12:04 pm

by absolutezero

Hariseldon58 wrote:absolutezero wrote:BT63 wrote:

Whilst not directed at me I do hold some OEICs,( far more ETFs)

Track an index not otherwise available as ETF, eg Vanguard Total US Market.

More established than the ETF equivalent eg Vanguard World Small Cap, more holdings, ie better representation, cheaper than the ETF equivalent.

Diversification of product type, in the event of a market failure, company failure, fraud etc

Invariably an accumulation version is available.

Clearly there are active OEICs without an ETF equivalent, may have an IT alternative though.

Food for thought. Thank you.

Re: What's in your portfolio and why?

Posted: October 21st, 2021, 10:25 am

by hiriskpaul

Hariseldon58 wrote:absolutezero wrote:BT63 wrote:

Whilst not directed at me I do hold some OEICs,( far more ETFs)

Track an index not otherwise available as ETF, eg Vanguard Total US Market.

More established than the ETF equivalent eg Vanguard World Small Cap, more holdings, ie better representation, cheaper than the ETF equivalent.

Diversification of product type, in the event of a market failure, company failure, fraud etc

Invariably an accumulation version is available.

Clearly there are active OEICs without an ETF equivalent, may have an IT alternative though.

I use OEIC trackers in our ISAs rather than ETFs. In addition to the above advantages, I can offer two more:

1) Dividends paid by ETFs are usually in a foreign currency. These are converted to GBP by the broker and the broker takes a cut. Only a few bps per year, but it all adds up. With OEICs, the fund manager converts dividends to GBP at inter Bank rates.

2) OEICs can often have lower charges and better tracking errors than ETFs. For example HSBC Europe ex-UK charges only 0.06%. The lowest charging equivalent ETF I know, from Vanguard, charges 0.10%

Some brokers charge ongoing platform fees for holding OEICs, which can outweigh any benefits, but our ISAs are with iWeb and they do not charge for holding OEICs, just a £5 per trade charge, which is the same for ETFs.