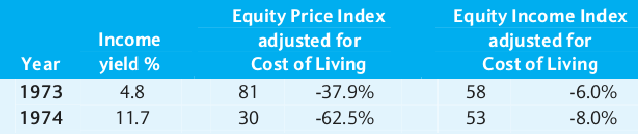

dealtn wrote:Check out those last 2 columns. That negative yield demonstrates how much purchasing power you are losing annually. If that can't be visualised look at the penultimate column of the price. Those bonds will all pay out at (real) 100, so even holding less than 10 years you are only getting 75% purchasing power, for the longer maturities less than half!

Only guaranteed to cost if held to maturity. If that is the sole intent then you have to blend with other assets such as stocks within this negative rates era (at other times you don't have to mix, as the bond itself can yield positive benefits). But many hold bonds for the insurance they provide against unexpected events/changes. If for instance inflation spiked to 5%, 10%, 20% ... or maybe more, then stocks might be repriced so that they are paying twice or more the dividend yield that they currently pay, and in that repricing the share price might halve or more (whatever). Bonds, both nominal and index linked provide insurance and/or cover against potential losses perhaps in other assets such as stocks. Nominal and index linked insure against different things, index linked for instance is more for a insurance against unexpected inflation, nominal bonds are more a insurance against deflation. That ILG inflation insurance comes at a cost presently, a negative real yield if held to maturity. But where if the insured against event does occur, such as unexpected high inflation, that might protect against some/most/all of losses in other assets value.

If your sole intent is to have a fixed inflation adjusted amount of value in a particular year, say £20,000 in 17 years time, then at current prices/values you have to load more into that bond, £25,000/whatever (haven't bothered run the calculation). If being employed as insurance then you have to assess how much insurance cover you want. If for instance you decide 33% index linked gilts is enough insurance against the rest being in stocks, then a -1.5% ILG cost is -0.5% relative to the total portfolio value. Then if stocks halve, ILG doubles you're still at 100% levels (but having seen the assets transition from 67% stock/33% ILG to being 33 stock/67 ILG).

The Permanent Portfolio choice of insurance level for instance is to hold 25% in each of stocks, gold, short dated gilts, long dated gilts. In effect it opts for gold over holding index linked gilts as spiking inflation cover. Which generally leads to a relatively stable ongoing portfolio value come what may. Or you can ride bareback, perhaps 100% stocks but at the risk that half of more of the value could vanish overnight. Countering that higher risk however is that stocks tend to reward more, so could relatively quickly recoup the loss, could take years, or could have achieved sufficient gains in earlier years that offset the declines/losses. If stocks pull 2x ahead for instance and then halve, in one respect there was no loss mathematically, however many actually mentally lock in paper gains so more often that will feel like a loss.

Yes if your objective was to provide £20,000 inflation adjusted value in 11 years time, another £20,000 in 12 years time ...etc. then at present you have to load in more than £20,000 into each index linked gilt that mature in 11 year, 12 year ...etc. At other times it has cost less to load up on such a ladder, where maybe you only had to load each rung with £15,000 or whatever. In that sense ILG's aren't good value at present, have been much better value in the past. But in other aspects ILG's and conventional bonds still have 'value', such as from a 'insurance' angle. And for unexpected inflation insurance typically the assets are ILG's and/or gold.