Dod101 wrote:As always it depends what the objective of the portfolio is. Tax wagging the dog's tail and all that. I live off my dividend income and currently generate rather more than I need to. I could look at transferring some holdings, not so much into a low income portfolio, but hopefully into a growth portfolio, rather harder to do in my experience. In any case at least with a relatively high income share, you have a good chance of getting a return even if it is taxed, with a possible bonus of a growth in the share price. The same can hardly be said for a low income share as you are already precluded from one source of return.

Dod

Total return is total return. Dividends can be as directed by the stock/fund, or DIY taken out of total return (at times and to the amounts of your own choosing).

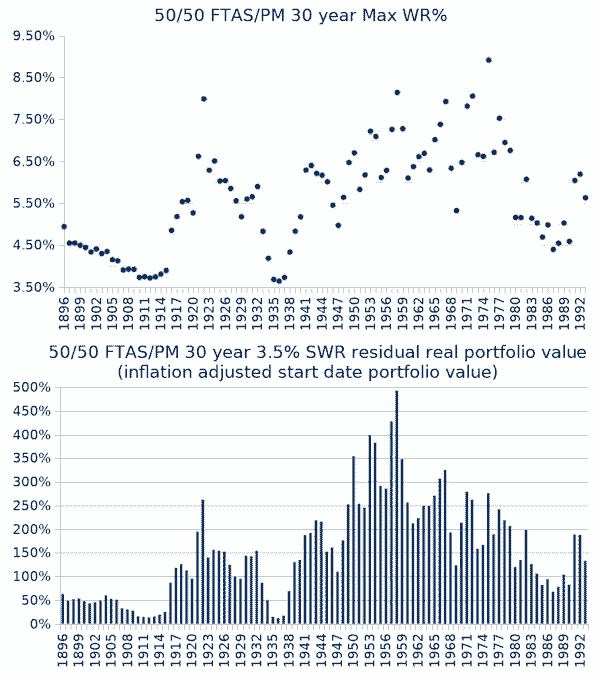

50/50 FT All Share/PM (precious metals), and historically a 30 year 3.66% SWR was supported. 3.66% of the start date portfolio value drawn as income for the first year, where that £££ amount is uplifted by inflation as the amount drawn as income in subsequent years, so a consistent/reliable (known) income each and every year. Dividends in contrast are more variable

US example,

BRK/Gold 50/50 3.5% SWR started in 1986, $500,000 initial portfolio value, $17,500 initial SWR value, and after income the portfolio value more recently stands at $17.4 million (grew at near 7% annualised real, 9.9% nominal). The continuation of the inflation adjusted $17,500 withdrawals (near $50,000 more recently) being less than 0.3% of the ongoing portfolio value. Yet over all of those years not a penny received in interest or dividends.

Inadvisable as even though BRK is a conglomerate, that is still a single stock risk factor, but you could split that with MKL (often referred to as being baby BRK, that also doesn't pay dividends) and/or other low/no dividend yield choices (FCIT that pays a relatively low dividend yield, as a world stock type proxy ...etc.).

Dividends come out of each firms bottom line. DIY dividends are sourced by other investors buying the shares that you sell, have no effect on the firm itself (other than a change of shareholder name entry on their register of shareholders). £100 of dividend paid out is £100 less the firm has, all else being equal the share price declines in reflection of that. In contrast £100 of stock value sold and the purchaser might be paying twice book-value (whatever) for those shares.

DIY dividends levelled to the amount and times of your own choosing are also more tax and cost efficient. It's nice to have some dividends however, perhaps up to your tax exempt/efficient allowances.

It's a lot easier to plan with a known figure. £10,000 of occupational pension, £10,000 of state pension, £20,000 of DIY dividends, all inflation adjusted, when your spending is £40,000/year. In contrast if stock dividends are £20,000 one year, but halve the next, £30,000 of income/£40,000 of spending and you have to sell £10,000 value of shares possibly at a time when share prices are down. DIY dividends sells share consistently, but that averages out, sometimes shares are sold at relatively higher prices, sometimes relatively lower prices, broadly washes.

Note that the 3.66% SWR figure is often rounded up to 4%, a low probability (relatively few historic cases) of that failing before 30 years, maybe only supporting 27 years. For a 65 year old retiree living to 92 is also a relatively low probability. There was also a relatively good probability of ending 30 years with the same or more in inflation adjusted terms as the start date portfolio value.

Gold (and/or art) is a asset for those who 'have enough' and are more interested in wealth preservation. Physical in-hand assets with no counter-party risk, that can be moved to less punitive regimes if/when the domestic regimes policies become more confiscatory. Proposals of wealth taxes more often ignore that will drive assets/wealth overseas - moved as soon as there is even a hint of such policies potentially rising, that includes stock value (T+2 time to liquidate and electronic transfer the sale proceeds). Which intends to burden the rest more. Better to have 1% paying a third of the total tax take, than see that flight and the rest having to fill that hole (having to pay 50% more in taxes). Even better still, US style, is to look to attract/develop wealth - ideally to 3% levels. But as LT/KK demonstrated, the UK prefers to totally stamp out such policies (with that can totally now flattened, not even kicked into the long grass, UK taxes have been doomed to rise to punitive levels - as favoured by Remainers - who opine if the UK suffers enough then it will rejoin the EU).

) approach, to reduce the impact of dividend taxes. I avoid companies which pay too high a dividend. I think that is sensible anyway.

) approach, to reduce the impact of dividend taxes. I avoid companies which pay too high a dividend. I think that is sensible anyway.