AEW UK REIT launched in May’15 amidst a flurry of listings by other small REITs, mostly concentrating on the undervalued regions.

AEWU is managed by AEW UK Investment Management which employs a team of 26. It is part of AEW Group, one of the world's largest real estate managers with EUR70.2bn of assets under management as at Sep’19.

https://www.aewukreit.com

The most recent trading Update on 16th January revealed these stats as at 31 Dec’19:

# Port = 35 regional properties

# Port Value = £195.8m

# Port split: IND – 48.5%; OFF – 23.1%; RET – 13.3%; Other 15.1%

# NAV = 97.24p/share

# Occupancy = 96.14%

# EPS for Q4’19 = 2.18p

# Q4’19 dividend = 2p/share (Targeted annual dividend = 8p/share)

# LTV = 26.3%

# Significant lettings ahead of estimated rental values

# Shares in Issue = 151.56m

# Borrowings: £51.5m to Oct’23 @ Libor + 1.4%. 90% hedged to max. Libor + 2%

https://uk.advfn.com/stock-market/londo ... i/81538274

So, in Feb’20, with everything in the garden looking rosy, the Company decided to launch a £20m equity raise at 97p/share. The endeavour was of course unfortunately timed, as the emerging Coronavirus scared off potential buyers, though they still managed to place 7.2m new shares.

On Black Monday (9th Mar’20) the shares dropped momentarily from 90p to a low of 83p, before recovering through that momentous day to close at 88p. Further progress today to 90p where the shares stand at an 8.2% discount and provide a covered yield of 8.9% - the highest in the sector.

Got a credit card? use our Credit Card & Finance Calculators

Thanks to gpadsa,Steffers0,lansdown,Wasron,jfgw, for Donating to support the site

AEW UK REIT (AEWU) - A covered 8.9% yield...

-

jackdaww

- Lemon Quarter

- Posts: 2081

- Joined: November 4th, 2016, 11:53 am

- Has thanked: 3203 times

- Been thanked: 417 times

Re: AEW UK REIT (AEWU) - A covered 8.9% yield...

fund charges seem a bit high at 2.44% which brings the return down somewhat .

-

PeanutsMolloy

- Posts: 9

- Joined: August 4th, 2021, 2:05 pm

- Has thanked: 20 times

- Been thanked: 7 times

Re: AEW UK REIT (AEWU) - A covered 8.9% yield...

Happy to have bought into AEWU in the summer last year, when I thought it offered a no-brainer yield of 12%pa and huge discount. Despite now trading close to NAV and 7.5%pa divi, it continues to be one of the best REITs out there IMHO and still offers decent value.

Its latest (30 Sept 21) quarterly presentation explains and, if you're not familiar with their strategy, I recommend sparing 44 mins to hear the story.

https://presentations.investormeetcompa ... b8a6916943

Its latest (30 Sept 21) quarterly presentation explains and, if you're not familiar with their strategy, I recommend sparing 44 mins to hear the story.

https://presentations.investormeetcompa ... b8a6916943

-

brightncheerful

- Lemon Quarter

- Posts: 2217

- Joined: November 4th, 2016, 4:00 pm

- Has thanked: 424 times

- Been thanked: 803 times

Re: AEW UK REIT (AEWU) - A covered 8.9% yield...

In my view, the regions are not undervalued. the higher yields for retail means they've gone ex-growth.

REIT share price investment potential is generally the difference between the current sp and the nav. Close or narrow the gap and it is then the challenge of increasing the nav, mostly achieved by yield compression. A property's fundamental potential for rental and/or capital growth is a separate issue.

REIT share price investment potential is generally the difference between the current sp and the nav. Close or narrow the gap and it is then the challenge of increasing the nav, mostly achieved by yield compression. A property's fundamental potential for rental and/or capital growth is a separate issue.

-

PeanutsMolloy

- Posts: 9

- Joined: August 4th, 2021, 2:05 pm

- Has thanked: 20 times

- Been thanked: 7 times

Re: AEW UK REIT (AEWU) - A covered 8.9% yield...

.... and AEWU cruises to a new ATH of 112p (recovering from Covid low <60p) and a small premium to NAV.

Capital raise coming no doubt, adding welcome firepower for a top investment team.

Capital raise coming no doubt, adding welcome firepower for a top investment team.

-

SKYSHIP

- Lemon Slice

- Posts: 479

- Joined: November 6th, 2016, 12:24 pm

- Has thanked: 2 times

- Been thanked: 556 times

Re: AEW UK REIT (AEWU) - A covered 8.9% yield...

A big write-up in IC Alpha - can be viewed through this link:

https://uk.advfn.com/cmn/fbb/thread.php ... &from=1231

https://uk.advfn.com/cmn/fbb/thread.php ... &from=1231

-

BullDog

- Lemon Quarter

- Posts: 2484

- Joined: November 18th, 2021, 11:57 am

- Has thanked: 2003 times

- Been thanked: 1213 times

Re: AEW UK REIT (AEWU) - Opinions?

Any views on AEWU here? Context - I have about 13 to 14% of total portfolio in two REITs, RGL and SOHO. Essentially offices and social housing.

Looking at AEWU, it's on a discount to NAV, not unusual for property companies of course. Pays a high, but covered yield. AEWU doesn't appear to have much if any overlap with the other REIT holdings.

I am thinking of bringing my total REIT exposure up to around the 20% mark. I don’t need the income to live off but would appreciate in the present inflationary environment deploying some spare cash to generate more income in the SIPP for the things I enjoy spending money on.

Any opinions on AEWU appreciated. Thanks.

Looking at AEWU, it's on a discount to NAV, not unusual for property companies of course. Pays a high, but covered yield. AEWU doesn't appear to have much if any overlap with the other REIT holdings.

I am thinking of bringing my total REIT exposure up to around the 20% mark. I don’t need the income to live off but would appreciate in the present inflationary environment deploying some spare cash to generate more income in the SIPP for the things I enjoy spending money on.

Any opinions on AEWU appreciated. Thanks.

-

monabri

- Lemon Half

- Posts: 8437

- Joined: January 7th, 2017, 9:56 am

- Has thanked: 1551 times

- Been thanked: 3449 times

Re: AEW UK REIT (AEWU) - A covered 8.9% yield...

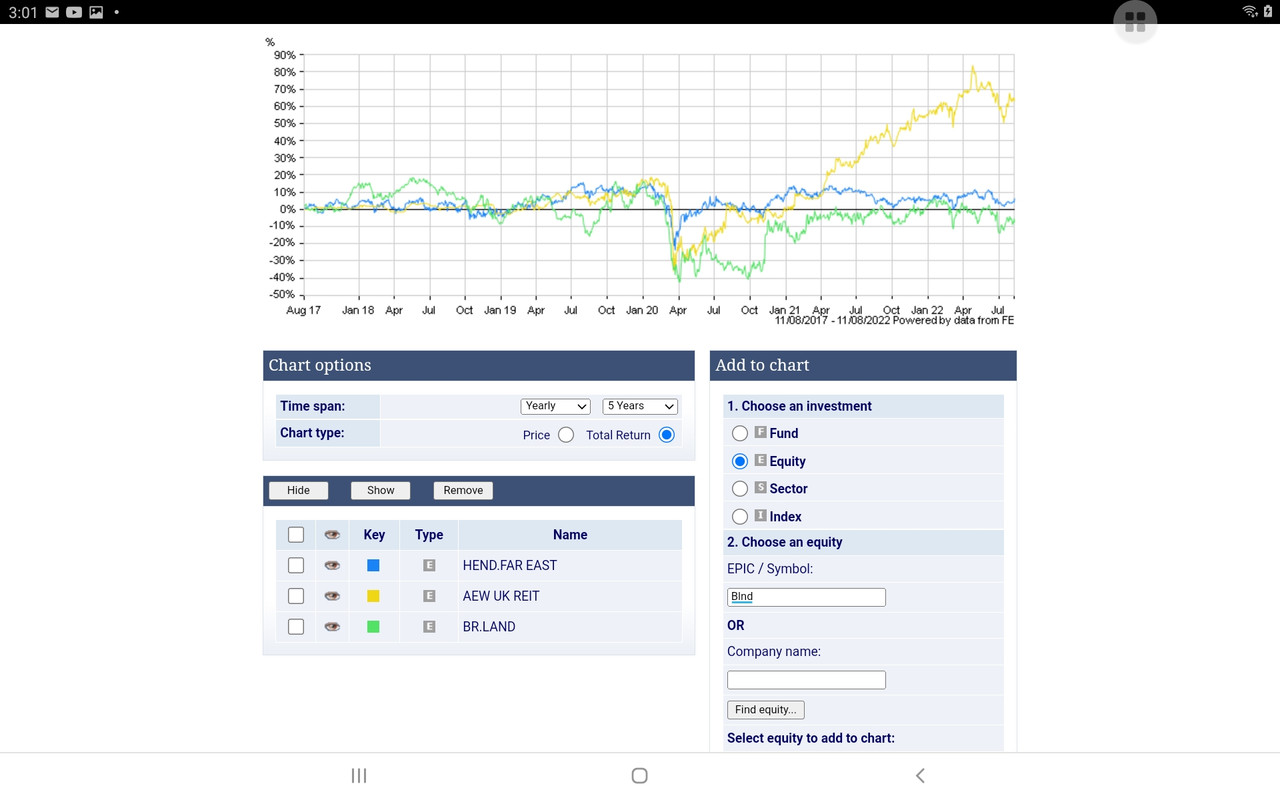

Looking back over the last 5 yrs it would have been a better choice than HFEL in terms of total return ( just thought I'd throw that one in  )

)

Will it continue to shine or ....? Why is it apparently doing so much better than BLND? I'd be cautious.

I note the gearing is reported at 22% so it might move quickly.

https://www.theaic.co.uk/companydata/0P0001604F

The dividend paid has been ( more or less) static.

Will it continue to shine or ....? Why is it apparently doing so much better than BLND? I'd be cautious.

I note the gearing is reported at 22% so it might move quickly.

https://www.theaic.co.uk/companydata/0P0001604F

The dividend paid has been ( more or less) static.

-

BullDog

- Lemon Quarter

- Posts: 2484

- Joined: November 18th, 2021, 11:57 am

- Has thanked: 2003 times

- Been thanked: 1213 times

Re: AEW UK REIT (AEWU) - A covered 8.9% yield...

monabri wrote:Looking back over the last 5 yrs it would have been a better choice than HFEL in terms of total return ( just thought I'd throw that one in

Will it continue to shine or ....? Why is it apparently doing so much better than BLND? I'd be cautious.

I note the gearing is reported at 22% so it might move quickly.

https://www.theaic.co.uk/companydata/0P0001604F

The dividend paid has been ( more or less) static.

Thanks Monabri. If that's the borrowing versus NAV, 22% is pretty modest for a REIT? I think?

Given we're heading into what the BoE thinks is going to be a sustained period of recession, I expect some pressure on property values and not exactly stellar growth of rental income. Not a short term holding I don't think were I to commit to buying.

Return to “REITs & Property Companies”

Who is online

Users browsing this forum: No registered users and 7 guests