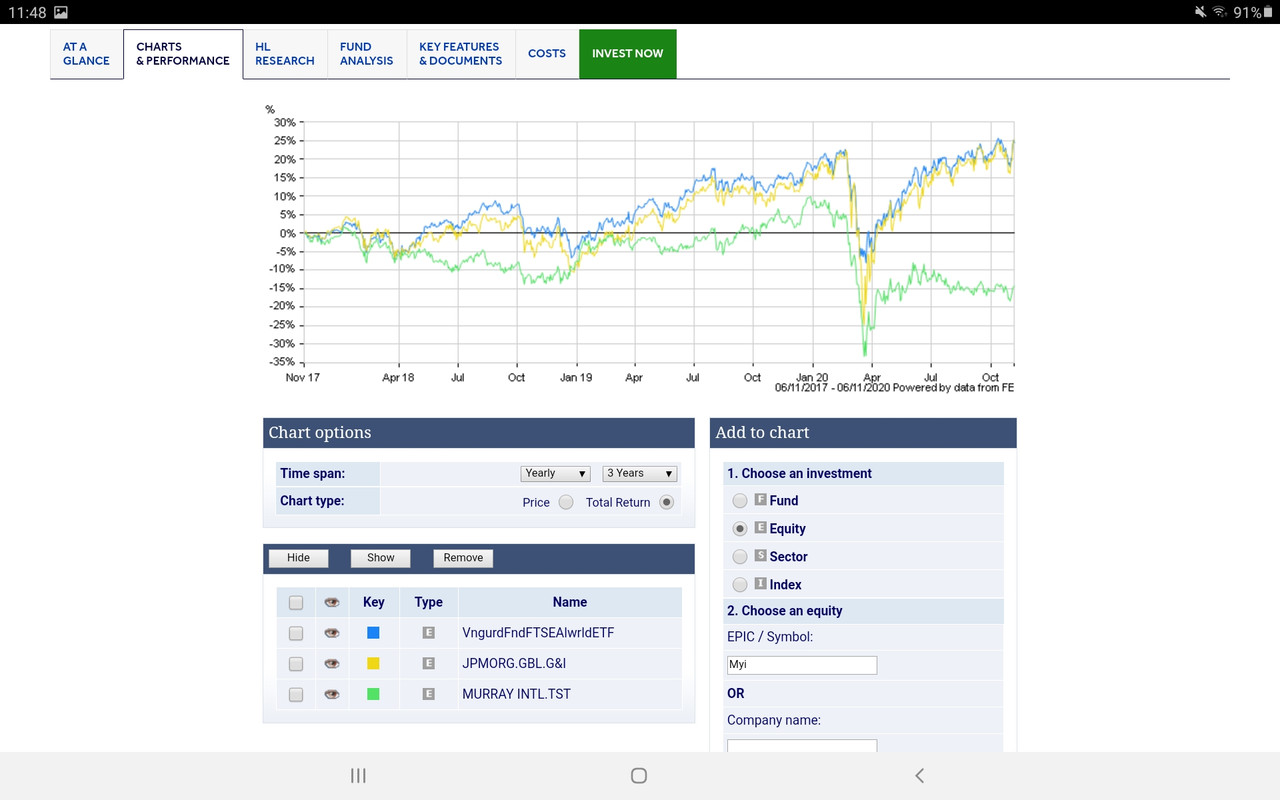

Murray International (MYI) is the largest global equity income trust, with a market cap of £1.2bn, and is, by some distance, the highest yielding. However, its long-term returns are far behind those of competing trusts.

Over 10 years, MYI has returned an average of 6.7% a year. Over one year, its net asset value return is almost 20% behind that of JPMorgan Global Growth and Income (JPGI), for example.

There is a material difference in the investment approaches of MYI and JPGI. MYI follows a traditional equity income style of seeking out companies with higher-than-average yields. JPGI invests in higher-growth but lower-yielding shares and makes up any shortfall in its revenue account by distributing capital.

However, given that valuations are much higher in the US than they are in emerging markets and growth prospects for emerging markets are better, I wonder whether this stance may pay off eventually.

I am struggling to see an immediate catalyst for a renaissance in the fortunes of what was for many years a powerhouse in the sector. That does not mean that we should write it off, however. If you think it will come right at some point over the next couple of years, the trust’s 5.6% yield pays you to wait.

https://citywire.co.uk/wealth-manager/n ... d/a1406111