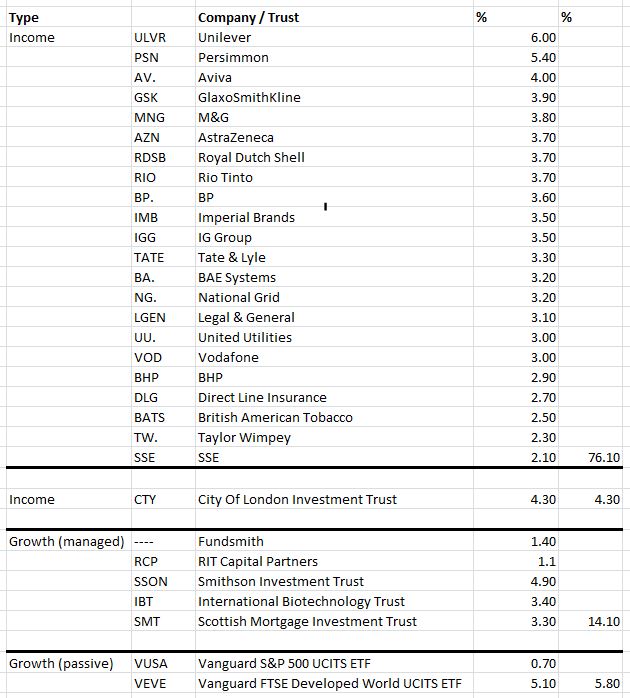

Stock name % Weight Sector

1 Fundsmith Equity Class I 29.8% Global - Hopefully continues its pattern of solid steady growth with no surprises.

2 Ruffer Investment Company Red Ptg Pref Shs GBP0.0001 28.7% [N/A] - Made a tidy profit off this and haven't quite got around to working out if it's a keep - hoping it will come in handy if the brown stuff properly hits the fan.

3 Capital Gearing Trust Plc Ord GBP0.25 20.7% [N/A] - Does what it says on the tin and I wouldn't have a hope in hell of playing the discount game the way they do.

4 UK Buffettology General 10.7% UK All Companies - Hopefully continues its pattern of solid steady growth with no surprises.

5 Smithson Investment Trust Plc Ord GBP 10.0% [N/A] - Hopefully continues its pattern of solid steady growth with no surprises.

6 Cash 0.1% [N/A]

I guess I'm trying to "barbell" between growth and preservation with hopefully minimal volatility along the way whilst accepting there has to be some in order to accumulate.