Prompted by this report I thought I'd start a new topic to follow aggregate trends rather than the parochial ones. Below are my skim read takeaways.

UN / Bloomberg : 2018 Global Trends in Renewable Energy Investment - report

http://fs-unep-centre.org/sites/default/files/publications/gtr2018v2.pdf

MONEY - 2017

Wind $107bn, solar $180bn, large hydro $45bn (mostly Baihetan dam, China), $103bn new fossil plan, $42bn nuclear

Now the developing countries are putting more money in to renewables capacity adds than developed, i.e. getting closer to fully commercial basis.

LEVELISED COSTS - 2017

"In the U.S., for instance, in 2017 the average LCOE without subsidy for PV without tracking was $54 per MWh, with onshore wind at $51 per MWh, versus gas-fired generation at $49 per MWh, coal at $66 and nuclear at $174". See graph on p17.

POWER & CAPACITY - 2017

61% of new capacity adds renewables

19% global gen capacity now renewable

12% actual generation is now renewable

VEHICLES & STORAGE - 2017

1.1 mln EVs sold (vs about 85 mln conventional)

$209/kWh for lithium ion battery packs

crossover point for unsubsidised EV to equal/beat conventional in mid 2020s on lifetime cost; late 2020s on purchase cost

regards, dspp

Got a credit card? use our Credit Card & Finance Calculators

Thanks to jfgw,Rhyd6,eyeball08,Wondergirly,bofh, for Donating to support the site

Renewable + conventional trends

-

dspp

- Lemon Half

- Posts: 5884

- Joined: November 4th, 2016, 10:53 am

- Has thanked: 5825 times

- Been thanked: 2127 times

-

dspp

- Lemon Half

- Posts: 5884

- Joined: November 4th, 2016, 10:53 am

- Has thanked: 5825 times

- Been thanked: 2127 times

Re: Renewable + conventional trends

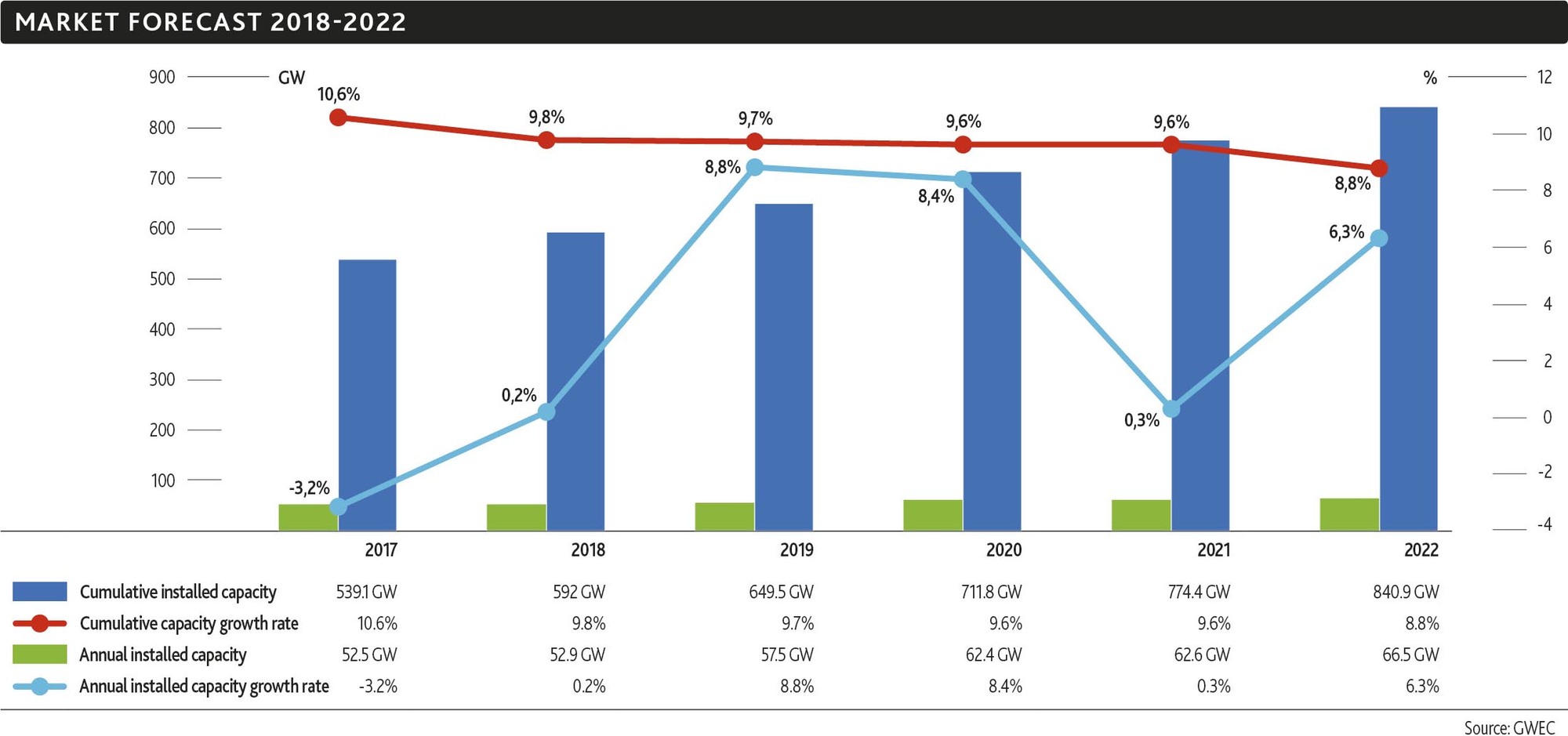

If you look at the latest annual GWEC report

http://gwec.net/cost-competitiveness-pu ... -in-front/

and in that look at the trend report

http://gwec.net/wp-content/uploads/2018 ... 8-2022.jpg

They are broadly predicting global wind installs will run flattish at 52-66 GW/yr .

Contrast that with the global PV trend

https://www.pv-magazine.com/2017/12/01/ ... modules-2/

which is basically climbing well above 100GW and showing no sign of decelerating and one has to wonder if there will in time be reduced demand for wind, i.e. will the flatlining wind market actually turn to a decline in due course. I can make the contrary argument that capacity factors are greater for wind, and that largescale deployment offshore of large rotor machines will further drive that, and that the wind/solar combi minimises storage costs, but nevertheless one has to wonder at the ways the trends are running.

regards, dspp

http://gwec.net/cost-competitiveness-pu ... -in-front/

and in that look at the trend report

http://gwec.net/wp-content/uploads/2018 ... 8-2022.jpg

{kind=link}

They are broadly predicting global wind installs will run flattish at 52-66 GW/yr .

Contrast that with the global PV trend

https://www.pv-magazine.com/2017/12/01/ ... modules-2/

which is basically climbing well above 100GW and showing no sign of decelerating and one has to wonder if there will in time be reduced demand for wind, i.e. will the flatlining wind market actually turn to a decline in due course. I can make the contrary argument that capacity factors are greater for wind, and that largescale deployment offshore of large rotor machines will further drive that, and that the wind/solar combi minimises storage costs, but nevertheless one has to wonder at the ways the trends are running.

regards, dspp

-

dspp

- Lemon Half

- Posts: 5884

- Joined: November 4th, 2016, 10:53 am

- Has thanked: 5825 times

- Been thanked: 2127 times

Re: Renewable + conventional trends

Bloomberg NEF report on 2018 renewable installs:

Increased capacity installed for slightly less money. Wind capacity growing slightly, money up slightly, shifting offshore (so capex/MW stable I guess, but capex/MWh improving) . Solar capacity growing strongly, money falling markedly, very good capex/MW increases. It is woth going to the link and taking a look at the two graphs. Solar and wind about equal in $ terms, but solar double wind in capacity terms. However since typical solar capacity factor is 10% and typical wind is 30+%, then wind is still beating solar in $/MWh terms. But solar can go in anywhere and in small chunks, whereas wind is location specific and is best done as big projects. So really nothing changes in the overall trajectory.

January 16, 2019

Solar commitments declined 24% in dollar terms even though there was record new photovoltaic capacity added, breaking 100GW barrier for the first time.

London and New York, January 16, 2019 – Global clean energy investment[1] totaled $332.1 billion in 2018, down 8% on 2017. Last year was the fifth in a row in which investment exceeded the $300 billion mark, according to authoritative figures from research company BloombergNEF (BNEF).

There were sharp contrasts between clean energy sectors in terms of the change in dollar investment last year. Wind investment rose 3% to $128.6 billion, with offshore wind having its second-highest year. Money committed to smart meter rollouts and electric vehicle company financings also increased.

However, the most striking shifts were in solar. Overall investment in that sector dropped 24% to $130.8 billion. Part of this reduction was due to sharply declining capital costs. BNEF’s global benchmark for the cost of installing a megawatt of photovoltaic capacity fell 12% in 2018 as manufacturers slashed selling prices in the face of a glut of PV modules on the world market.

That surplus was aggravated by a sharp change in policy in China in mid-year. The government acted to cool that country’s solar boom by restricting access for new projects to its feed-in tariff. The result of this, combined with lower unit costs, was that Chinese solar investment plunged 53% to $40.4 billion in 2018.

etc

2018 results:

https://about.bnef.com/blog/clean-energ ... lion-2018/

2019 predictions:

https://about.bnef.com/blog/transition- ... ions-2019/

Increased capacity installed for slightly less money. Wind capacity growing slightly, money up slightly, shifting offshore (so capex/MW stable I guess, but capex/MWh improving) . Solar capacity growing strongly, money falling markedly, very good capex/MW increases. It is woth going to the link and taking a look at the two graphs. Solar and wind about equal in $ terms, but solar double wind in capacity terms. However since typical solar capacity factor is 10% and typical wind is 30+%, then wind is still beating solar in $/MWh terms. But solar can go in anywhere and in small chunks, whereas wind is location specific and is best done as big projects. So really nothing changes in the overall trajectory.

January 16, 2019

Solar commitments declined 24% in dollar terms even though there was record new photovoltaic capacity added, breaking 100GW barrier for the first time.

London and New York, January 16, 2019 – Global clean energy investment[1] totaled $332.1 billion in 2018, down 8% on 2017. Last year was the fifth in a row in which investment exceeded the $300 billion mark, according to authoritative figures from research company BloombergNEF (BNEF).

There were sharp contrasts between clean energy sectors in terms of the change in dollar investment last year. Wind investment rose 3% to $128.6 billion, with offshore wind having its second-highest year. Money committed to smart meter rollouts and electric vehicle company financings also increased.

However, the most striking shifts were in solar. Overall investment in that sector dropped 24% to $130.8 billion. Part of this reduction was due to sharply declining capital costs. BNEF’s global benchmark for the cost of installing a megawatt of photovoltaic capacity fell 12% in 2018 as manufacturers slashed selling prices in the face of a glut of PV modules on the world market.

That surplus was aggravated by a sharp change in policy in China in mid-year. The government acted to cool that country’s solar boom by restricting access for new projects to its feed-in tariff. The result of this, combined with lower unit costs, was that Chinese solar investment plunged 53% to $40.4 billion in 2018.

etc

2018 results:

https://about.bnef.com/blog/clean-energ ... lion-2018/

2019 predictions:

https://about.bnef.com/blog/transition- ... ions-2019/

-

TheMotorcycleBoy

- Lemon Quarter

- Posts: 3246

- Joined: March 7th, 2018, 8:14 pm

- Has thanked: 2226 times

- Been thanked: 588 times

Re: Renewable + conventional trends

Hi,

Apologies if this is the wrong thread to pose this question but it looked like a reasonable choice; and that is, are firms like BP and Shell looking at all into, research and then gradual diversification into non-fossil fuel based energy sources? Or as entities (do people think they) will they dwindle either as demand (climate change concerns) or supply (diminishing resources) effect their size and profitability?

thanks Matt

Apologies if this is the wrong thread to pose this question but it looked like a reasonable choice; and that is, are firms like BP and Shell looking at all into, research and then gradual diversification into non-fossil fuel based energy sources? Or as entities (do people think they) will they dwindle either as demand (climate change concerns) or supply (diminishing resources) effect their size and profitability?

thanks Matt

-

TheMotorcycleBoy

- Lemon Quarter

- Posts: 3246

- Joined: March 7th, 2018, 8:14 pm

- Has thanked: 2226 times

- Been thanked: 588 times

Re: Renewable + conventional trends

Ahh... some stuff here about Shell's investment in other energy sources

https://www.fool.com/investing/2018/07/ ... shell.aspx

https://www.fool.com/investing/2018/07/ ... shell.aspx

-

dspp

- Lemon Half

- Posts: 5884

- Joined: November 4th, 2016, 10:53 am

- Has thanked: 5825 times

- Been thanked: 2127 times

Re: Renewable + conventional trends

TMB,

That's a fair TMF-USA article re RDSB, but it is only a limited view in my opinion.

The institutional culture within Shell is very long term and aware of the context in which they operate, and open to doing things differently, and doing different things (unlike, say, Exxon) but there is not unanimity on the approach at any given moment. This is a healthy thing in my opinion as it avoids sterile groupthink, or the danger of domination by charismatic leaders that have occurred in some peers (BP, I'm looking at you). Shell is also more independent and global in thought and not a foreign/national policy tool to any way near the same extent as (say) ENI or Total. Those are my observations of ways of assessing culture in the majors. You can make similar qualitative assessments about the mid tier and the minors as well.

The downside of this is that Shell sometimes make a big & wrong call (entering coal, nuclear, forestry* to name but a few) but the upside is that they have the mental honesty to reverse the decision as pathways become clearer (and remember, sometimes the position is just for learning and/or hedging purposes, so the unwind may be egg-on-the-face but still profitable). So they are well aware of the trends in the energy sector and are themselves continually figuring out how to make a lowish risk transition. This is by no means a new discussion item in Shell and is pretty much slide 1 of day 1 training within Shell's long term workforce. It is worth reading the Shell quarterly updates & slide decks etc to get some more insight rather than depending on TMF-USA on this.

A lot of people & companies in the oil sector are dead set against transition, some to the point of denial of any of the rationales. This makes them uninvestable. Others may be capricious movers, which makes them higher risk plays. If looking at the global vertically-integrated majors you want to do serious quantitative analysis, then best to start simply by looking at their gas exposure vs their oil exposure, and by looking at the type of oil they have on their books (heavy, light, etc) and their reserves position.

Simply investing well in this area is a tough call - so not unreasonably investing with the transition in mind squares the challenge. It is a very valid discussion item but one we are unlikely to 'settle' here on TLF Personally one of the reasons my portfolio is tilted towards RDSB is because I see the transition position/time/manner debate within RDSB as being conducted more thoughtfully than in the others, and I do not see good opportunities for me to (as an individual) invest in renewables (yet) with a risk/reward profile that I find attractive.

Personally one of the reasons my portfolio is tilted towards RDSB is because I see the transition position/time/manner debate within RDSB as being conducted more thoughtfully than in the others, and I do not see good opportunities for me to (as an individual) invest in renewables (yet) with a risk/reward profile that I find attractive.

regards, dspp

* these examples may be before your time, and have long since been exited

That's a fair TMF-USA article re RDSB, but it is only a limited view in my opinion.

The institutional culture within Shell is very long term and aware of the context in which they operate, and open to doing things differently, and doing different things (unlike, say, Exxon) but there is not unanimity on the approach at any given moment. This is a healthy thing in my opinion as it avoids sterile groupthink, or the danger of domination by charismatic leaders that have occurred in some peers (BP, I'm looking at you). Shell is also more independent and global in thought and not a foreign/national policy tool to any way near the same extent as (say) ENI or Total. Those are my observations of ways of assessing culture in the majors. You can make similar qualitative assessments about the mid tier and the minors as well.

The downside of this is that Shell sometimes make a big & wrong call (entering coal, nuclear, forestry* to name but a few) but the upside is that they have the mental honesty to reverse the decision as pathways become clearer (and remember, sometimes the position is just for learning and/or hedging purposes, so the unwind may be egg-on-the-face but still profitable). So they are well aware of the trends in the energy sector and are themselves continually figuring out how to make a lowish risk transition. This is by no means a new discussion item in Shell and is pretty much slide 1 of day 1 training within Shell's long term workforce. It is worth reading the Shell quarterly updates & slide decks etc to get some more insight rather than depending on TMF-USA on this.

A lot of people & companies in the oil sector are dead set against transition, some to the point of denial of any of the rationales. This makes them uninvestable. Others may be capricious movers, which makes them higher risk plays. If looking at the global vertically-integrated majors you want to do serious quantitative analysis, then best to start simply by looking at their gas exposure vs their oil exposure, and by looking at the type of oil they have on their books (heavy, light, etc) and their reserves position.

Simply investing well in this area is a tough call - so not unreasonably investing with the transition in mind squares the challenge. It is a very valid discussion item but one we are unlikely to 'settle' here on TLF

regards, dspp

* these examples may be before your time, and have long since been exited

-

TheMotorcycleBoy

- Lemon Quarter

- Posts: 3246

- Joined: March 7th, 2018, 8:14 pm

- Has thanked: 2226 times

- Been thanked: 588 times

Re: Renewable + conventional trends

Many thanks for this reply, Dave,

Yes, the impression I got from the article was that Shell were, perhaps, quite forward looking.

I wasn't aware of these, but I guess, many firms make ventures down side-alleys, and not all of those end up in dictating the "correct" path. But so as long as they can recover from the odd U-turn, then no lasting problem....

Thanks - yes will do.

We have no oilies or energy providers (except Nat Grid NG.). In fact our foli arguably lacks diversity in oil/gas, pharma (we just have Bioventix BVXP which is more bio-tech than pharma), and media/IT. Sorry to get a tad off topic there....

I've tried to stick to just highish OM, and ROCE firms (with at least *some* dividend, yes you and I have had this discussion in the past ). As such we've got several "manufacturers" or niche suppliers (like Spirax). I'd like to put some energy (oil and renewables) in there, but struggled to find one I'm happy with. RDS is low on the OM and ROCE front, but definitely pays a decent DY, and if future earnings get protected by means of gradual diversification (renewables) then it could be worth a punt for us, I think.

). As such we've got several "manufacturers" or niche suppliers (like Spirax). I'd like to put some energy (oil and renewables) in there, but struggled to find one I'm happy with. RDS is low on the OM and ROCE front, but definitely pays a decent DY, and if future earnings get protected by means of gradual diversification (renewables) then it could be worth a punt for us, I think.

Ditto. I (briefly) looked at JLEN (John Laing Environment Services) the IT, but then I'd have to research ITs - a whole other investment ballgame, and furthermore (at first glance at their spec sheet) nothing really shouted at me, to buy a chunk.

So a holding in RDSB for us looks increasingly interesting.

thanks again

Matt

dspp wrote:TMB,

The institutional culture within Shell is very long term and aware of the context in which they operate, and open to doing things differently, and doing different things (unlike, say, Exxon) but there is not unanimity on the approach at any given moment. This is a healthy thing in my opinion as it avoids sterile groupthink, or the danger of domination by charismatic leaders that have occurred in some peers (BP, I'm looking at you). Shell is also more independent and global in thought and not a foreign/national policy tool to any way near the same extent as (say) ENI or Total. Those are my observations of ways of assessing culture in the majors. You can make similar qualitative assessments about the mid tier and the minors as well.

Yes, the impression I got from the article was that Shell were, perhaps, quite forward looking.

dspp wrote:The downside of this is that Shell sometimes make a big & wrong call (entering coal, nuclear, forestry* to name but a few) but the upside is that they have the mental honesty to reverse the decision as pathways become clearer (and remember, sometimes the position is just for learning and/or hedging purposes, so the unwind may be egg-on-the-face but still profitable).

I wasn't aware of these, but I guess, many firms make ventures down side-alleys, and not all of those end up in dictating the "correct" path. But so as long as they can recover from the odd U-turn, then no lasting problem....

dspp wrote: So they are well aware of the trends in the energy sector and are themselves continually figuring out how to make a lowish risk transition. This is by no means a new discussion item in Shell and is pretty much slide 1 of day 1 training within Shell's long term workforce. It is worth reading the Shell quarterly updates & slide decks etc to get some more insight rather than depending on TMF-USA on this.

Thanks - yes will do.

dspp wrote:Personally one of the reasons my portfolio is tilted towards RDSB is because I see the transition position/time/manner debate within RDSB as being conducted more thoughtfully than in the others,

We have no oilies or energy providers (except Nat Grid NG.). In fact our foli arguably lacks diversity in oil/gas, pharma (we just have Bioventix BVXP which is more bio-tech than pharma), and media/IT. Sorry to get a tad off topic there....

I've tried to stick to just highish OM, and ROCE firms (with at least *some* dividend, yes you and I have had this discussion in the past

dspp wrote: and I do not see good opportunities for me to (as an individual) invest in renewables (yet) with a risk/reward profile that I find attractive.

Ditto. I (briefly) looked at JLEN (John Laing Environment Services) the IT, but then I'd have to research ITs - a whole other investment ballgame, and furthermore (at first glance at their spec sheet) nothing really shouted at me, to buy a chunk.

So a holding in RDSB for us looks increasingly interesting.

thanks again

Matt

-

dspp

- Lemon Half

- Posts: 5884

- Joined: November 4th, 2016, 10:53 am

- Has thanked: 5825 times

- Been thanked: 2127 times

Re: Renewable + conventional trends

Yes, I have looked at JLEN a few times courtesy of the various folk who have prompted it. I cannot see much upside however so have done nothing so far.

regards, dspp

regards, dspp

-

TheMotorcycleBoy

- Lemon Quarter

- Posts: 3246

- Joined: March 7th, 2018, 8:14 pm

- Has thanked: 2226 times

- Been thanked: 588 times

Re: Renewable + conventional trends

dspp wrote:Yes, I have looked at JLEN a few times courtesy of the various folk who have prompted it. I cannot see much upside however so have done nothing so far.

regards, dspp

I just took another look. It does currently have about 5.68% DY

From here:

https://jlen.com/wp-content/uploads/201 ... tsheet.pdf

6.31p (div) / 111p (current price) = 5.68%

So perhaps one to keep in mind (for me possibly).

-

TheMotorcycleBoy

- Lemon Quarter

- Posts: 3246

- Joined: March 7th, 2018, 8:14 pm

- Has thanked: 2226 times

- Been thanked: 588 times

-

TheMotorcycleBoy

- Lemon Quarter

- Posts: 3246

- Joined: March 7th, 2018, 8:14 pm

- Has thanked: 2226 times

- Been thanked: 588 times

Re: Renewable + conventional trends

Of interest?

Shell goes green as it rebrands UK household power supplier

https://uk.reuters.com/article/uk-shell ... KKCN1R50OL

Shell goes green as it rebrands UK household power supplier

https://uk.reuters.com/article/uk-shell ... KKCN1R50OL

-

dspp

- Lemon Half

- Posts: 5884

- Joined: November 4th, 2016, 10:53 am

- Has thanked: 5825 times

- Been thanked: 2127 times

Re: Renewable + conventional trends

'Coal is on the way out': study finds fossil fuel now pricier than solar or wind

Around 75% of coal production is more expensive than renewables, with industry out-competed on cost by 2025 [in USA]

etc https://www.theguardian.com/environment ... ergy-study

Around 75% of coal production is more expensive than renewables, with industry out-competed on cost by 2025 [in USA]

etc https://www.theguardian.com/environment ... ergy-study

-

richfool

- Lemon Quarter

- Posts: 3529

- Joined: November 19th, 2016, 2:02 pm

- Has thanked: 1208 times

- Been thanked: 1294 times

Re: Renewable + conventional trends

dspp wrote:Yes, I have looked at JLEN a few times courtesy of the various folk who have prompted it. I cannot see much upside however so have done nothing so far.

regards, dspp

To clarify, I hold JLEN mainly for the dividend yield and to gain exposure to alternative asset classes which hopefully are less correlated to equities, (rather than for actual growth).

-

Nimrod103

- Lemon Half

- Posts: 6625

- Joined: November 4th, 2016, 6:10 pm

- Has thanked: 977 times

- Been thanked: 2329 times

Re: Renewable + conventional trends

dspp wrote:'Coal is on the way out': study finds fossil fuel now pricier than solar or wind

Around 75% of coal production is more expensive than renewables, with industry out-competed on cost by 2025 [in USA]

etc https://www.theguardian.com/environment ... ergy-study

When I last looked at this, as I recall, the calculation of the cost of electricity generated from coal in these types of comparisons included the cost of separating and disposing of the CO2, which AIUI has not yet been done commercially. The Guardian article just says the cost of coal generation includes pollution control measures. Any comment?

-

dspp

- Lemon Half

- Posts: 5884

- Joined: November 4th, 2016, 10:53 am

- Has thanked: 5825 times

- Been thanked: 2127 times

Re: Renewable + conventional trends

Nimrod103 wrote:dspp wrote:'Coal is on the way out': study finds fossil fuel now pricier than solar or wind

Around 75% of coal production is more expensive than renewables, with industry out-competed on cost by 2025 [in USA]

etc https://www.theguardian.com/environment ... ergy-study

When I last looked at this, as I recall, the calculation of the cost of electricity generated from coal in these types of comparisons included the cost of separating and disposing of the CO2, which AIUI has not yet been done commercially. The Guardian article just says the cost of coal generation includes pollution control measures. Any comment?

Nimrod,

This particular analysis does not include CO2 costs, either as a negative externality cost, or as a carbon capture and storage (CCS) cost. So it is giving the easiest possible playing field to coal, though it does include some fairly minor and standard pollution control costs (i.e. the cost of fitting/operating/maintaining various acid-rain type scrubbers). In fact in this study the playing field is tilted in favor of coal by not loading the coal plant with repayment of capital for the initial build, i.e. stranded capital is ignored. It is a plant-specific study for all plants & areas, not some sort of aggregate study.

It is a pretty good study, worth reading,

"the going-forward costs for the vast majority of coal plants fall between $33 – 111 / megawatt-hours (MWh). Costs in 2018 for solar are more tightly clustered, between $28 – 52 / MWh, while wind costs vary more widely based on locational resource quality, falling between $13 – 88 / MWh"

https://energyinnovation.org/wp-content ... _FINAL.pdf

Basically it is saying that coal is dead. Except perhaps for coking coal. This is the same conclusion that the Indians have reached, which is why Indian coal mines & power plants are crashing in value right now https://www.cnbc.com/2019/02/20/reuters ... ssell.html . Quite simply coal is being out-competed worldwide by unsubsidised wind & solar.

Intermittency / despatchable power and storage are being solved at a fast enough rate that we can see, that by the time the stranded assets are worked out the system, the replacement storage schemes will be sufficient. At least that is my view of the data.

regards, dspp

-

dspp

- Lemon Half

- Posts: 5884

- Joined: November 4th, 2016, 10:53 am

- Has thanked: 5825 times

- Been thanked: 2127 times

Re: Renewable + conventional trends

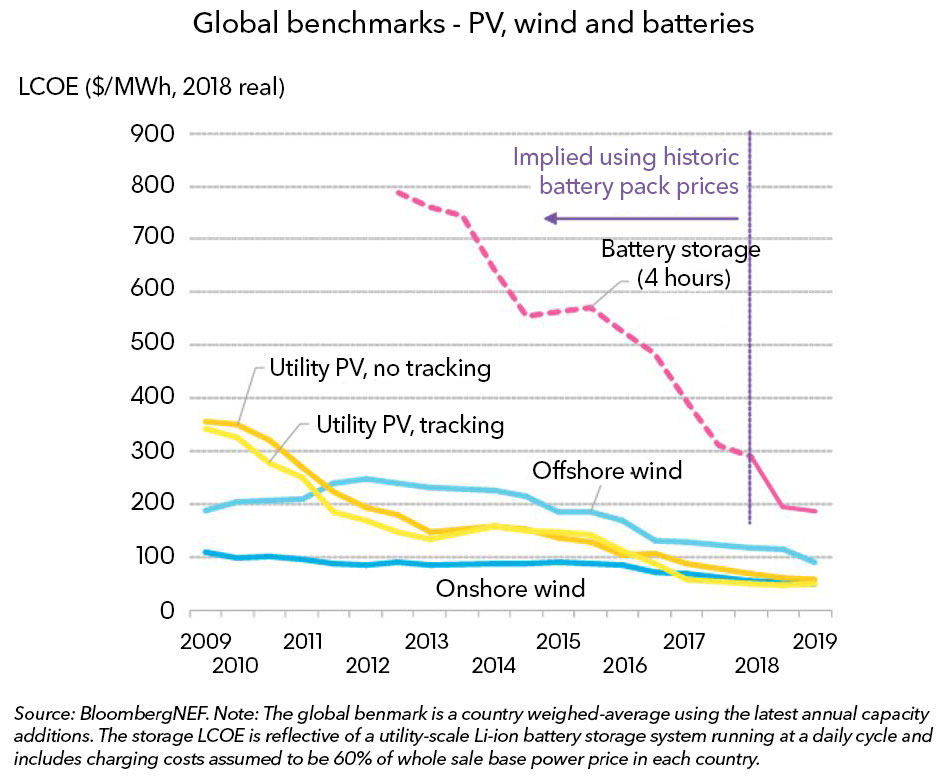

Battery Power’s Latest Plunge in Costs Threatens Coal, Gas

The latest analysis by research company BloombergNEF (BNEF) shows that the benchmark levelized cost of electricity,[1] or LCOE, for lithium-ion batteries has fallen 35% to $187 per megawatt-hour since the first half of 2018. Meanwhile, the benchmark LCOE for offshore wind has tumbled by 24%.

Onshore wind and photovoltaic solar have also gotten cheaper, their respective benchmark LCOE reaching $50 and $57 per megawatt-hour for projects starting construction in early 2019, down 10% and 18% on the equivalent figures of a year ago.

.... Batteries co-located with solar or wind projects are starting to compete, in many markets and without subsidy, with coal- and gas-fired generation for the provision of ‘dispatchable power’ that can be delivered whenever the grid needs it (as opposed to only when the wind is blowing, or the sun is shining).

etc https://about.bnef.com/blog/battery-pow ... -coal-gas/

Take a look at the graph below, then check data in my post of 25-Mar-2019 giving LCOE of coal at $33-111 /MWh, then project trend decline a little bit, and you can see that conventional legacy fossil plant is likely to become stranded assets very soon.

- dspp

The latest analysis by research company BloombergNEF (BNEF) shows that the benchmark levelized cost of electricity,[1] or LCOE, for lithium-ion batteries has fallen 35% to $187 per megawatt-hour since the first half of 2018. Meanwhile, the benchmark LCOE for offshore wind has tumbled by 24%.

Onshore wind and photovoltaic solar have also gotten cheaper, their respective benchmark LCOE reaching $50 and $57 per megawatt-hour for projects starting construction in early 2019, down 10% and 18% on the equivalent figures of a year ago.

.... Batteries co-located with solar or wind projects are starting to compete, in many markets and without subsidy, with coal- and gas-fired generation for the provision of ‘dispatchable power’ that can be delivered whenever the grid needs it (as opposed to only when the wind is blowing, or the sun is shining).

etc https://about.bnef.com/blog/battery-pow ... -coal-gas/

Take a look at the graph below, then check data in my post of 25-Mar-2019 giving LCOE of coal at $33-111 /MWh, then project trend decline a little bit, and you can see that conventional legacy fossil plant is likely to become stranded assets very soon.

- dspp

-

dspp

- Lemon Half

- Posts: 5884

- Joined: November 4th, 2016, 10:53 am

- Has thanked: 5825 times

- Been thanked: 2127 times

Re: Renewable + conventional trends

Germany generated 54.5 percent of electricity from renewable energy in March 2019.

The Fraunhofer data shows wind power generated 34.4 percent of the energy mix, solar power at 7.3 percent with the remaining 12.8 percent coming from hydropower and biomass.... Germany has been steadily adding renewables into its generation mix as part of the Energiewende, which translates to Energy Transition. The company has pledged a low-carbon, nuclear-free future and has been installing both onshore and offshore wind and solar at a quick pace. ...

Despite the influx of renewables, however, carbon emissions for the country have not fallen as it has had to burn more coal than ever in order to keep the grid stable after closing its nuclear units in 2011 in response to the Fukushima disaster.

https://www.renewableenergyworld.com/ar ... march.html

https://www.energy-charts.de/ren_share_ ... y&year=all

Italy must more than double its capacity to store electricity

Italy may need as many as 6 gigawatts of storage by 2030 to balance a boom in renewables. .. Most of the country’s 4.8 gigawatts of storage capacity currently comes from pumped hydro plants, where water is stored in a reservoir and then allowed to flow over a generation turbine during times of peak power demand, ..“This is an opportunity not only for the energy sector but also for agriculture,” Ferraris said. “We need sites to store water for agriculture. There could be multiple uses for these sites.’’ + more comments saying that hydro storage cheaper than battery storage at the moment

https://www.renewableenergyworld.com/ar ... id=2410249

The Fraunhofer data shows wind power generated 34.4 percent of the energy mix, solar power at 7.3 percent with the remaining 12.8 percent coming from hydropower and biomass.... Germany has been steadily adding renewables into its generation mix as part of the Energiewende, which translates to Energy Transition. The company has pledged a low-carbon, nuclear-free future and has been installing both onshore and offshore wind and solar at a quick pace. ...

Despite the influx of renewables, however, carbon emissions for the country have not fallen as it has had to burn more coal than ever in order to keep the grid stable after closing its nuclear units in 2011 in response to the Fukushima disaster.

https://www.renewableenergyworld.com/ar ... march.html

https://www.energy-charts.de/ren_share_ ... y&year=all

Italy must more than double its capacity to store electricity

Italy may need as many as 6 gigawatts of storage by 2030 to balance a boom in renewables. .. Most of the country’s 4.8 gigawatts of storage capacity currently comes from pumped hydro plants, where water is stored in a reservoir and then allowed to flow over a generation turbine during times of peak power demand, ..“This is an opportunity not only for the energy sector but also for agriculture,” Ferraris said. “We need sites to store water for agriculture. There could be multiple uses for these sites.’’ + more comments saying that hydro storage cheaper than battery storage at the moment

https://www.renewableenergyworld.com/ar ... id=2410249

-

dspp

- Lemon Half

- Posts: 5884

- Joined: November 4th, 2016, 10:53 am

- Has thanked: 5825 times

- Been thanked: 2127 times

Re: Renewable + conventional trends

Nimrod,

I figured I'd put my response to (viewtopic.php?f=16&t=11847) here as it is something that affects both conventional & renewable trends. Also I took the time to dig out & refresh data I last looked at back in the days of TMF. Back then I was projecting forwards to the 50/50 point, now we are at it - see below.

From BP Statistical Review 2018 (i.e. data to end 2017) you can pull out the table of primary energy by fuel type (p9) see (https://www.bp.com/en/global/corporate/ ... nergy.html) and do a few sums:

From Hook et al, CERA, etc (see table 4 of https://royalsocietypublishing.org/doi/ ... .2012.0448) we know that typical post peak giant field declines are 6.5%. So in order for oil to maintain its existing share of global energy it has to commercially invest in, and technically successfully find & develop 6.5% each year.

But in addition to that, in the one year period 2017>2018 oil supply (and therefore demand, as at this scale storage in negligible) also increased by 0.5% of the global total energy production as you can see in the calculation in the table above. So really oil has to add 6.5% + 0.5% = 7.0% just for supply to match demand. If that investment was not made then oil price would rise in due course (ignoring, for simplicity, all the confounding factors).

But what you can also see is that in the same one year period renewables supply increased by 0.5% of the global total energy production, and they too cannot be stored at scale so that is also a demand increase. In other words if it were not for the presence of renewables growth then (all things equal) oil would have had to rise 6.5% + 0.5% + 0.5% = 7.5%. Now in most industries the bigger the challenge, the bigger the price effect.

So we can already see that renewables is currently taking 0.5% / 7.5% = 7% of the load in terms of filling the gap created each year by the combination of (replace oil reservoir decline + satisfy increased energy demand). That will already be having an effect on oil price. You could say that renewables are equal to oil (50/50) in filling the growth need (0.5% vs 0.5%), plus of course that oil has to do even more (6.5%) just to keep level.

If you look at p43 of the BP Stat Review you will see that renewables have gone from about 40 mtoe in 1997 to 486 mtoe in 2017. In pricing terms they have gone from being utterly insignificant to being quite significant. In due course they will become dominant.

Now look at the steepness of the bottom left chart on (p43) and look at the corresponding renewables growth rate (far bottom right, p48) which is 17% yoy. If that rate is kept up for the next 10-years then renewables will grow from 486 mtoe to 2336 mtoe. If we assume that the global energy demand continues to grow at 1.9% yoy then primary energy demand will be 16,305 mtoe in 2027 (personally I think it will be less, but let's be conservative in this calculation). So in 2027 renewables will have increased from 3.6% (2017) to 14% of global energy. Assume hydro stays at 7% and nukes at 4% and non-carbon would then be 25% of total energy.

Looking at the 2027 annual capacity add figures, the renewables capacity add would be 339 mtoe, which represents either 2.1% of the 2027 global energy figure, or 2.5% of the 2017 figure. Either way you can see that oil could easily be in decline (unless coal is taking the hit for a decade) and that - at that point - about a third of the annual reservoir decline figure would not be replaced. That has got to have an effect on oil price at some point (imagine the shape of the futures curve at that moment ....).

Personally I see the overall transition going a bit faster than this, but my opinion is that coal will take the hit for about a decade (i.e. 28% share whittled down at 2% per year) which means that the real crunch point for oil comes in 2037, not 2027. In the meantime it is a reasonable bet to hold oil shares that have good quality (i.e. short-dated) reservoirs. So nice light oils in high porosity & high permeability. Gas rich is good unless stranded. Heavy oils are to be avoided. Low EROEI reservoirs are to be avoided (so minimise shale exposure) and nice energetic reservoirs are to be preferred. But the world is a forwards-looking place and so oilpatch valuations will get depressed in advance, plus of course there will be the peak oil volatility to cope with.

I hope that gives a sense of where my thinking is. It certainly affects my own investment choices. And looking around the patch you can see it affecting the majors and their decisions.

regards, dspp

I figured I'd put my response to (viewtopic.php?f=16&t=11847) here as it is something that affects both conventional & renewable trends. Also I took the time to dig out & refresh data I last looked at back in the days of TMF. Back then I was projecting forwards to the 50/50 point, now we are at it - see below.

From BP Statistical Review 2018 (i.e. data to end 2017) you can pull out the table of primary energy by fuel type (p9) see (https://www.bp.com/en/global/corporate/ ... nergy.html) and do a few sums:

From Hook et al, CERA, etc (see table 4 of https://royalsocietypublishing.org/doi/ ... .2012.0448) we know that typical post peak giant field declines are 6.5%. So in order for oil to maintain its existing share of global energy it has to commercially invest in, and technically successfully find & develop 6.5% each year.

But in addition to that, in the one year period 2017>2018 oil supply (and therefore demand, as at this scale storage in negligible) also increased by 0.5% of the global total energy production as you can see in the calculation in the table above. So really oil has to add 6.5% + 0.5% = 7.0% just for supply to match demand. If that investment was not made then oil price would rise in due course (ignoring, for simplicity, all the confounding factors).

But what you can also see is that in the same one year period renewables supply increased by 0.5% of the global total energy production, and they too cannot be stored at scale so that is also a demand increase. In other words if it were not for the presence of renewables growth then (all things equal) oil would have had to rise 6.5% + 0.5% + 0.5% = 7.5%. Now in most industries the bigger the challenge, the bigger the price effect.

So we can already see that renewables is currently taking 0.5% / 7.5% = 7% of the load in terms of filling the gap created each year by the combination of (replace oil reservoir decline + satisfy increased energy demand). That will already be having an effect on oil price. You could say that renewables are equal to oil (50/50) in filling the growth need (0.5% vs 0.5%), plus of course that oil has to do even more (6.5%) just to keep level.

If you look at p43 of the BP Stat Review you will see that renewables have gone from about 40 mtoe in 1997 to 486 mtoe in 2017. In pricing terms they have gone from being utterly insignificant to being quite significant. In due course they will become dominant.

Now look at the steepness of the bottom left chart on (p43) and look at the corresponding renewables growth rate (far bottom right, p48) which is 17% yoy. If that rate is kept up for the next 10-years then renewables will grow from 486 mtoe to 2336 mtoe. If we assume that the global energy demand continues to grow at 1.9% yoy then primary energy demand will be 16,305 mtoe in 2027 (personally I think it will be less, but let's be conservative in this calculation). So in 2027 renewables will have increased from 3.6% (2017) to 14% of global energy. Assume hydro stays at 7% and nukes at 4% and non-carbon would then be 25% of total energy.

Looking at the 2027 annual capacity add figures, the renewables capacity add would be 339 mtoe, which represents either 2.1% of the 2027 global energy figure, or 2.5% of the 2017 figure. Either way you can see that oil could easily be in decline (unless coal is taking the hit for a decade) and that - at that point - about a third of the annual reservoir decline figure would not be replaced. That has got to have an effect on oil price at some point (imagine the shape of the futures curve at that moment ....).

Personally I see the overall transition going a bit faster than this, but my opinion is that coal will take the hit for about a decade (i.e. 28% share whittled down at 2% per year) which means that the real crunch point for oil comes in 2037, not 2027. In the meantime it is a reasonable bet to hold oil shares that have good quality (i.e. short-dated) reservoirs. So nice light oils in high porosity & high permeability. Gas rich is good unless stranded. Heavy oils are to be avoided. Low EROEI reservoirs are to be avoided (so minimise shale exposure) and nice energetic reservoirs are to be preferred. But the world is a forwards-looking place and so oilpatch valuations will get depressed in advance, plus of course there will be the peak oil volatility to cope with.

I hope that gives a sense of where my thinking is. It certainly affects my own investment choices. And looking around the patch you can see it affecting the majors and their decisions.

regards, dspp

-

dspp

- Lemon Half

- Posts: 5884

- Joined: November 4th, 2016, 10:53 am

- Has thanked: 5825 times

- Been thanked: 2127 times

Re: Renewable + conventional trends

UK power grid to be 'zero-carbon-capable' says operator

The grid may start dropping its need for natural gas power for short periods in about 2025, coinciding with coal’s complete phaseout. The system wants to be “zero-carbon capable” by then, said Julian Leslie, head of national control at National Grid Plc’s electricity system operator.

While natural gas regularly provides more than half of the U.K.’s electricity, increasing wind and solar power output means the need for the fossil fuel is sometimes very low, falling below a quarter of usage on windy days.

To eliminate the need for fossil fuels, the U.K. will need to begin thinking about how to replace gas stations straight away, Leslie said. New market rules to retain transparency and competitive tension, as well as calls for tenders as early as next year for new types of equipment will also be needed.

“All of those things need to happen in order to make the zero-carbon-in-2025 aspiration happen,” Leslie said in a telephone interview. “In 2025, it may just be for half an hour, it may just be for an hour. Then gradually, in the years that follow, that time period will grow and grow.”

“Given the U.K.’s battery storage current and future capacity, I would have imagined the issue would have to be addressed closer to the 2030s,” ...

etc https://www.renewableenergyworld.com/ar ... id=2415856

The grid may start dropping its need for natural gas power for short periods in about 2025, coinciding with coal’s complete phaseout. The system wants to be “zero-carbon capable” by then, said Julian Leslie, head of national control at National Grid Plc’s electricity system operator.

While natural gas regularly provides more than half of the U.K.’s electricity, increasing wind and solar power output means the need for the fossil fuel is sometimes very low, falling below a quarter of usage on windy days.

To eliminate the need for fossil fuels, the U.K. will need to begin thinking about how to replace gas stations straight away, Leslie said. New market rules to retain transparency and competitive tension, as well as calls for tenders as early as next year for new types of equipment will also be needed.

“All of those things need to happen in order to make the zero-carbon-in-2025 aspiration happen,” Leslie said in a telephone interview. “In 2025, it may just be for half an hour, it may just be for an hour. Then gradually, in the years that follow, that time period will grow and grow.”

“Given the U.K.’s battery storage current and future capacity, I would have imagined the issue would have to be addressed closer to the 2030s,” ...

etc https://www.renewableenergyworld.com/ar ... id=2415856

-

dspp

- Lemon Half

- Posts: 5884

- Joined: November 4th, 2016, 10:53 am

- Has thanked: 5825 times

- Been thanked: 2127 times

Re: Renewable + conventional trends

Global Wind Energy Council (GWEC) unveiled the 14th edition of its Global Wind Report

The report provides a comprehensive global view of both the onshore and offshore wind energy sector. Data in the report confirms that 2018 was a positive year for the wind industry, with 51.3 GW of new installations. Market-based mechanisms, such as auctions, tenders and Green Certificates were the main drivers behind new installations in 2018. Looking ahead, the market outlook for the global wind industry is strong, said the group. GWEC Market Intelligence expects over 300 GW of new capacity to be added in the next five years.

etc https://www.renewableenergyworld.com/ar ... id=2415856

If you look at my post #212769 in this thread on on 4-Apr-2019 (viewtopic.php?f=16&t=11176) you will see that I did some calcs using a 17% yoy renewables growth rate which I took from BP Stats Review and which is the 20-year average growth rate. The 300GW of capacity adds in the next 5-years that GWEC is forecasting represents a 23% yoy growth rate. Since wind is the dominant new renewables generator then, if at best, the transition is likely to go faster than my earlier calculation. At worst these numbers are consistent.

Both sets of numbers indicate that investments in large scale storage, PV, and wind could be interesting (absent boom & bust ...) and that legacy fossil plant makers might be less so. A brave stock picker can tell me which way to go ! E.g. https://www.offshorewind.biz/2019/04/09 ... ructuring/ Senvion restructuring. These days you have to be a BIG player to survive. If you are a latecomer you have to spend a lot of extra $$$, time, risk to fight your way to the table.

regards, dspp

The report provides a comprehensive global view of both the onshore and offshore wind energy sector. Data in the report confirms that 2018 was a positive year for the wind industry, with 51.3 GW of new installations. Market-based mechanisms, such as auctions, tenders and Green Certificates were the main drivers behind new installations in 2018. Looking ahead, the market outlook for the global wind industry is strong, said the group. GWEC Market Intelligence expects over 300 GW of new capacity to be added in the next five years.

etc https://www.renewableenergyworld.com/ar ... id=2415856

If you look at my post #212769 in this thread on on 4-Apr-2019 (viewtopic.php?f=16&t=11176) you will see that I did some calcs using a 17% yoy renewables growth rate which I took from BP Stats Review and which is the 20-year average growth rate. The 300GW of capacity adds in the next 5-years that GWEC is forecasting represents a 23% yoy growth rate. Since wind is the dominant new renewables generator then, if at best, the transition is likely to go faster than my earlier calculation. At worst these numbers are consistent.

Both sets of numbers indicate that investments in large scale storage, PV, and wind could be interesting (absent boom & bust ...) and that legacy fossil plant makers might be less so. A brave stock picker can tell me which way to go ! E.g. https://www.offshorewind.biz/2019/04/09 ... ructuring/ Senvion restructuring. These days you have to be a BIG player to survive. If you are a latecomer you have to spend a lot of extra $$$, time, risk to fight your way to the table.

regards, dspp

Return to “Oil & Gas & Energy (Sector & Companies)”

Who is online

Users browsing this forum: No registered users and 22 guests